Menu

Login

Mr. Cooper - Loan # [protected]

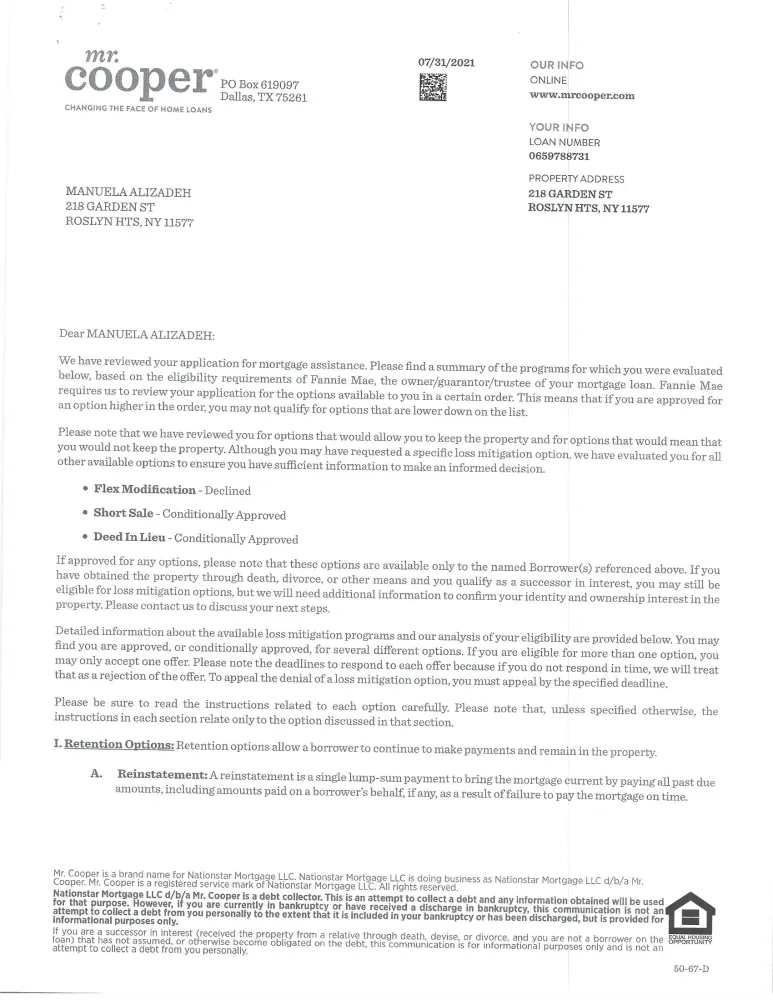

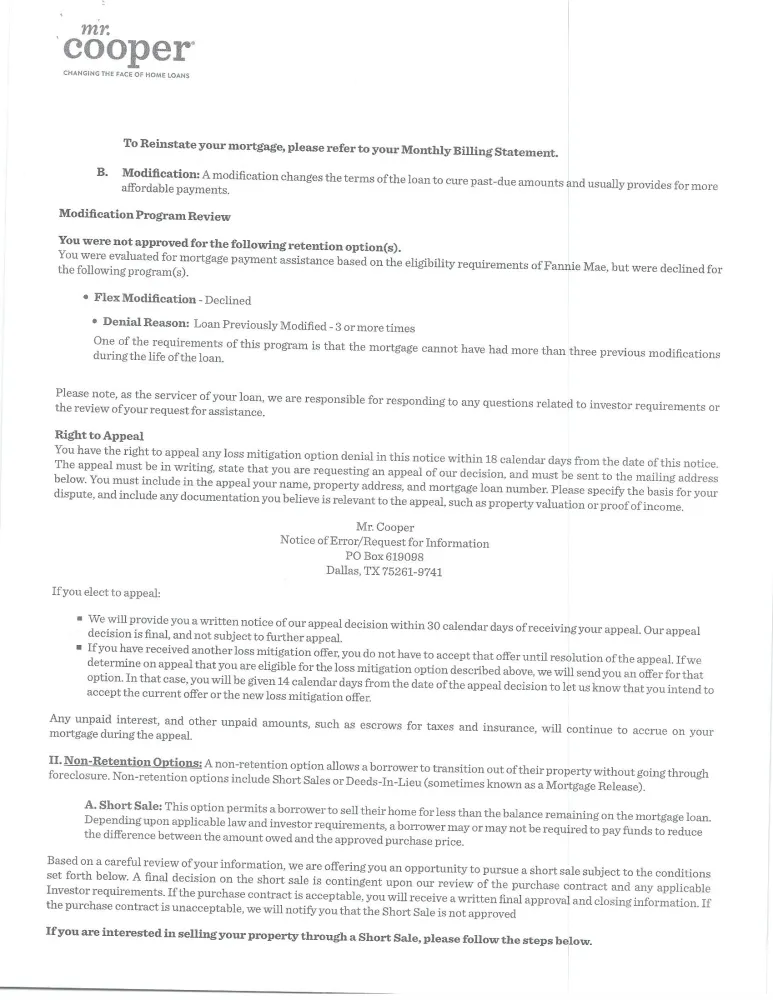

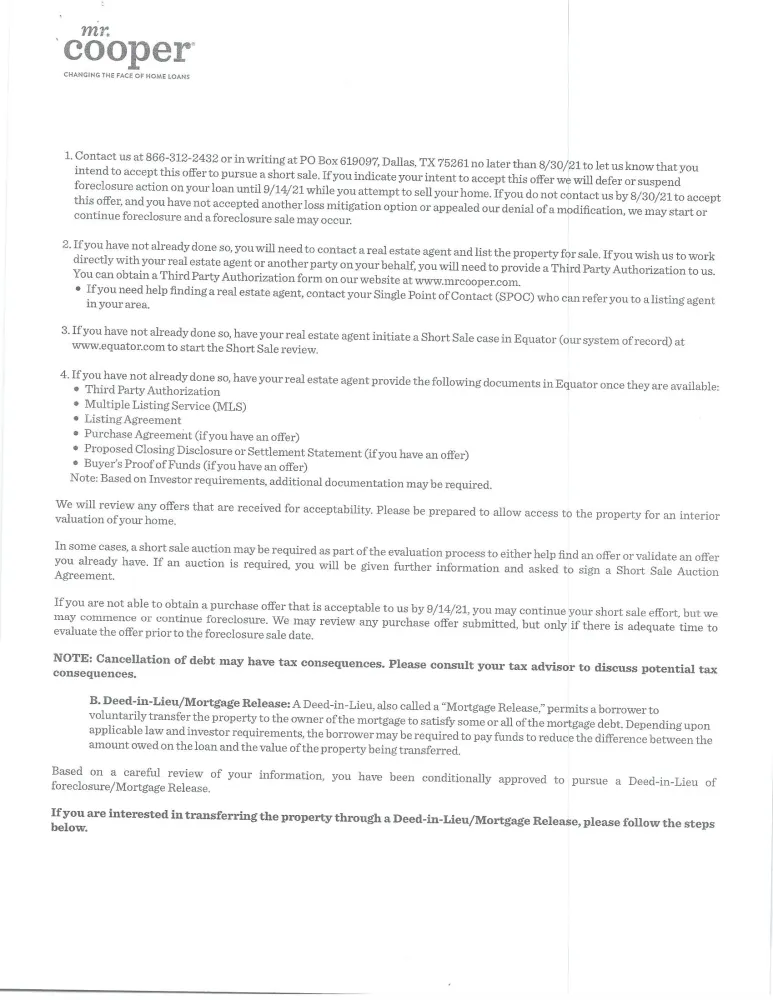

Mr. Cooper denied a Loan Modification after Forbearance ended. The day after forbearance ended I received a denial letter that my only options were a lump sum payment or a short sale or a deed in Lieu.

I have owned this home since 1993 and refuse to give it up after so much money spent in order to maintain it plus this is my home!. My child was born here and I always made a good income until the pandemics hit, hence the request for forbearance.

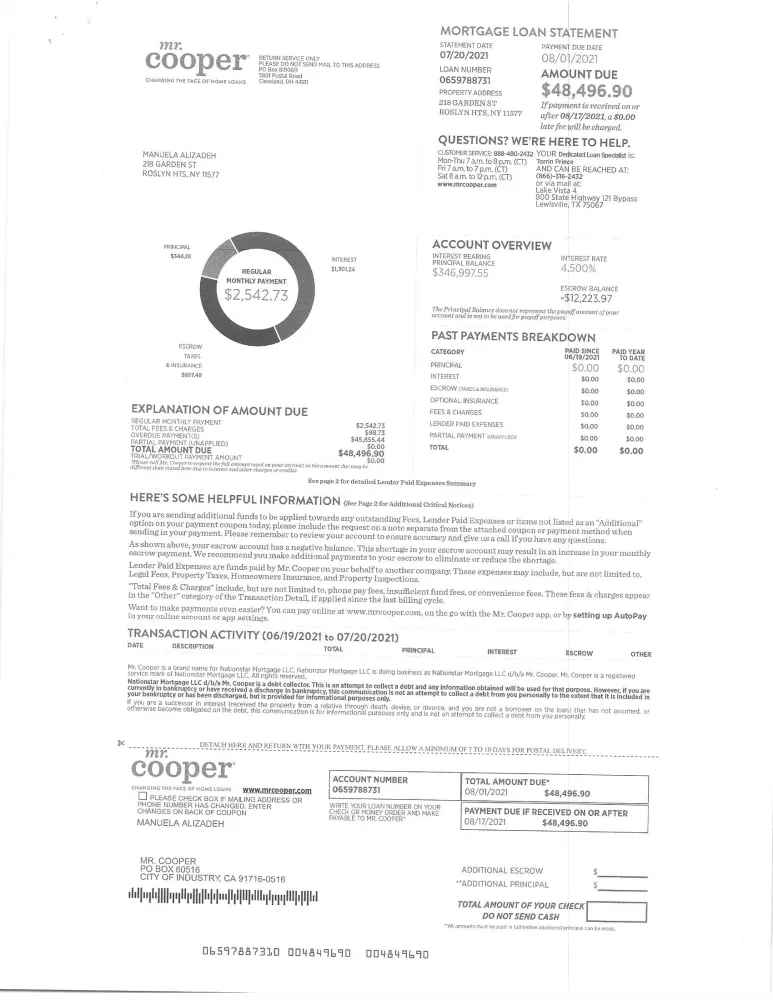

I have a good income now - $87, 00 plus my son can be a co-signer. He makes $52, 000. A total of $139, 000 is more than sufficient to pay a mortgage of $2, 600 plus additional escrow payments of $1, 000 per month until current.

When I entered the forbearance in April of 2020, Mr. Cooper agents hinted that the amount unpaid would go towards the end of the loan. Mr. Cooper is servicing a Fannie Mae loan, which has a lot of federal restrictions, inclusive of NOT requesting a lump sum payment. I am the perfect candidate for a loan modification. There is no reason for this denial. Mr.Cooper only intends to steal my property rather than work with a serious worker who loves her home. After losing 2 relatives to COVID, they are attempting to take away my only security. After living and caring for this home for 28 years, I will not accept this terrible offense from Mr. Cooper! I am a Special Education home teacher for children with autism and was unable to work during the pandemics. Children with autism require a specific type of in-person instruction. I am also an evaluator.

Desired outcome: I want a loan modification, whereas, the forbearance amount is placed towards the end of the loan

Omg… I am having the same issue with Mr. Cooper, There is no communication, no one to speak to aside from customer service agents who give incorrect info. My single point of contact I have yet to speak to & another cs agent told me they are the same as my single point of contact & said they issue the names of the customer service agents as single point of contacts because they have to assign a name so they are in compliance with certain laws & guidlines. It’s ridiculous, I had income documents rejected time after time & then denied for a modification. They are suppose to offer a streamlined flex modification trial period once u are 90 days or more delinquent with no documentation needed & once the 3 month trial period payments are made on time they proceed with underwriting that is the Freddie Mac guidlines for servicers. My forbearance ended august 31st & I have not made the 3 payments to see if they offer me the modification but they have not so I don’t know what to do. My understanding from other sources is that u can make a payment plan to pay extra with current mortgage payments to catch up the forbearance or you can put the forbearance at the end of the loan due at the end of loan term or when u sell or refinance. You can google Freddie Mac flex modification guidelines & it is a detailed guide that servicers are to go by.

I have the same issue, I applied for a loan mod, I wasn't advised that the loan mod was denied without any explanation, It was my understanding that the payments would go to the end of the loan, I wasn't offered anything at all. there is a mortgage grant coming but it hasn't been funded as of yet, I am going to appeal the denial and see what happens

This is ? exactly what they did to me also. Their agents make you think that a deferral is available and then at the tail end of the forbearance period in September 2021, After calling for weeks trying to get a hold of my “dedicated loan specialist” I could not get a representative on the phone! I was finally told she no longer worked there….I demanded a manager and again nothing..This went on for over a week. They purposely avoid calls and intently string homeowners along, lie, waited until after the Cares Act ended to drop the bomb that they only want a LUMP Sum payment. They have agents that pass you along to other completely useless and ignorant agents and then the day I put my foot down and demanded to be escalated and try and resolve the balance they put a male on who aggressively stated I had to pay the lump sum for be put into foreclosure! These thugs have no shame and blatantly lie and set up homeowners for potential failure just to steal their properties. They know exactly how to train their agents to mislead, lie, and with intent to foreclose. They purposely let time erode because they know how to let the timelines run until you have no options. They are the worst of the worst you could ever entounter and cannot trust anything they say and they refuse to put anything in writing. I wonder why?

They need to be held responsible for their fraudulent acts and willful distress they have placed on so many homeowners.

One day they will each pay the price for their actions

Have you received any resolution from them?

Is there any recourse I can pursue toward my mortgage company, that used unethical and immoral practices as leverage to gain financially. Situatio is so similar more to add. Iron clad evidence, 3 years worth. Current conjured forbearance, being used as leverage ends tomorrow. I'm going to inform them of evidence, dear them to foreclosure, and tell recourse that someone tells me today.