Mr. Cooper reviews and complaints 567

Keywords

mortgage payment company loan late payment account department escrow taxes check house credit insurance refinance foreclosure documentation agents call family interest ratesNewest Mr. Cooper reviews and complaints

loan modifcation process misrepresentation by lender

I began the Loan Modification Process in July 2010 to save my property since I had encountered severe financial difficulties. After months of submitting documentation, having them misplace the docs, having them not respond, not provide accurate information, provide bad advice, and spending hours on the phone in trying to have the process approved, I found out yesterday that my house was foreclosed on 10/14/2010. This was after they said that they would stop any foreclosure proceedings during the loan mod process and not to make any additional payments until then since it was not necessary. I had on multiple attempts told them over the past few months that if the loan mod were not going to be approved for any reason that I wanted to try to sell the property via a Short Sale and then if that didn't work process a deed in lieu of foreclosure, just anything to prevent the foreclosure process. They said I couldn't do a short sale until I was behind on payments and then they would have to approved it but not to seek it since the loan mod was being processed. On 9/24/2010 I submitted the paperwork as requested for the loan officer to postpone any foreclosure until the loan mod was approved, faxed the docs as requested, and they told me not to worry that they had received the docs and the foreclosure process would be postponed. I reiterated to please tell me if it would not go through so I could try to sell the property on a short sale. Yesterday, 10/20/10 I called since a notice was on the house saying a realtor had the property due to a Sheriff Sale (Foreclosure). I was so confused so called the office and could not reach a representative and then was transfered multiple times to the wrong departments, then was sent to a voice mail box that was always full. On/ 10/20/10, I called again until I reached a rep for over 2 hours and they said the loan mod was not approved due to other laws that they just found out and that it was foreclosed and there was nothing I could do. So, I cried for awhile and called the Short Sale Dept and they said I could still do the Short Sale which would relieve me of most of the debt but that my credity rating would still be stated as a Foreclosure even if the property sells on the Short Sale and there is no balance due. The Foreclosure rating would then remain as a negative on my credit report for 7 years. If I want to redeem the property since it is occupied in Michigan I have 6 months to redeem the preoperty if I pay the back payments, the attorneys fees, and other fees which is over $6, 000 at a minimum, plus my credit is still then bad because of the late payments through the six month redemption period. After months of dealting with Nationstar and having every representative that gave advice not be familiar with the Making Home Affordable Laws (HUD) and providing incorrect information, and months of phone calls, submitting and resubmitting documentation and then to no avail having my home going to foreclosure due to incorrect advice from Nationstar and thus being distraught, mentally and physically exhausted from trying to save my home I hope that the Making Home Affordable Program (HUD), FDIC, FTC, and the State Attorney General look into their corrupt practices that detroy homeowner's lives. Please if you value your home do not listen to Nationstar's Advice seek out a HUD Counselor, or if at all possible obtain another mortgage with a more reputable company that is knowledgeable on mortgage practices and the new lawas on saving your home. I have been crying for two days and trying to work so I don't lose my job due to being so distraught and trying to focus to complete work. Nationstar is as close to being a criminal as any company could possibly get. I am going to attempt to start a Class Action Lawsuit against them for misrepresentation to mortgage holders thus causing the loss of their homes. Hopefully, many others will follow and have cases that support what they have been doing to customers.

The complaint has been investigated and resolved to the customer’s satisfaction.

Aurora Loan Services is a Fraud

I had a similar experience with Aurora, as all of you. Aurora has done all it could not to help my husband and I keep our home. Here is my story:

I purchased my home September 2006. The loan was with First Magnus. It was set up as an 80/20 loan. Shortly thereafter my loan with First Magnus was sold to Aurora Loan Services. I am not sure which bank corresponds with Aurora Loan Services. In April 2007, I lost my job and was not able to pay for my mortgage. I contacted Aurora and explained the situation to them. I asked them for a work up or a differed payment for a few months until I would find another job. They refused to help me, because I was making my payments on time. A few days later I was served with Foreclosure papers.

I struggled to make payments on time. In 2008 out of desperation I contacted Majestic Properties for a loan modification. I hired them. Their fee was $2000 and I paid them $1500 down for this service and gave them power of attorney to communicate with Aurora on my behalf for a loan modification. They did very little for me, as they were telling me that Aurora was unwilling to cooperate with them.

In March of 2009 my husband had a triple bypass surgery. Now he is on Dialysis. I provided Aurora with the hardship letter and proof from his medical records from his Doctors.

I was keeping in touch with Majestic Properties office on a weekly basis.

Finally after almost three years and many letters and phone calls, not to mention numerous foreclosure cancelations, Aurora agreed on a work up based on a three month trial period. Aurora sent me the paper work. I took it to Majestic Properties to have assistance with this process. I filled out the paper work and submitted it to Aurora. I was to pay them $840 a month for three months after which my case would be re-evaluated. I made my monthly mortgage payments to Aurora on time. After the initial three month trial period they re-evaluated the case, I re-submitted all the paper work they asked for all over again, and I was approved for three more months. Again I was making my monthly mortgage payments on time. I was cooperating with them fully.

When the second set of three month trial period was up, I re-submitted the paper work they had asked for again. The paper work was faxed from Majestic Properties while I was in their office. The loan modification associate was on the phone with an Aurora representative. The fax went through but the Aurora representative stated they did not receive it. This was not the first time that Aurora representatives stated they did not receive pertinent information from me, which I had indeed sent them. I was always gathering information and running around trying to give them the appropriate information as they requested.

It is important to mention that while I was in the middle of this loan modification process Aurora placed a note on my garage door with date for the trustee sale, on two separate occasions. Why would they do that, if I was complying with this work up, and making payments? They made it impossible for me to continue with the modification.

Finally Aurora was no longer cooperating with the modification, and I had no choice but to start a short sale process. Mean while the two loan modification specialists that I was dealing with at Majestic Properties formed their own company named Foreclosure Short Sale Specialists LLC.

Shortly thereafter they started having financial difficulties and they were no longer handling my short sale case. They had helped me a lot with many foreclosure cancelations and submitting paper work to Aurora, but there was never a successful loan modification done by them, nor a short sale. Seeing how Foreclosure Short Sale Specialist LLC was no longer representing me with the short sale, I contacted my Realtor and he contacted Aurora and started the Short Sale process all over again.

The other day I found out that Foreclosure Short Sale Specialists LLC defrauded many people. They charged them lots of money for short sale and loan modifications and never did a thing for them. Their office is closed now and they fled town.

November 2009 we put the house up for short sale and my Realtor sold it in June 2010 for half the price I bought it for.

I had every intention to keep my home and cooperate with Aurora. My only options were short sale and foreclosure. The loan was solely on my husband’s name and I did not want his credit to be ruined, by foreclosing. His credit was adversely affected anyway because of Aurora was cooperating and dragged the process out for many years.

This was a difficult time for me because my husband had just had major heart surgery and I was not able to inform him of the stress Aurora was inflicting on me. My husband was not to be under any type of stress after his triple bypass surgery.

Banks took money from tax payers in bail outs to help those affected by the economical crisis yet they did nothing to help us stay in our home, there for if there is an Attorney out there considering class action law suits I would like to be included. You can reach me at my e-mail address [protected]@yahoo.com.

The complaint has been investigated and resolved to the customer’s satisfaction.

I am having a hard time and certainly suprise how our govermnet allow this crimminal act to happen

robbed me of my house

Nationstar totally robbed me out of my house. Mid Aug. i made payment arrangements to pay 3 payments before Sept. 1. Well i called Nationstar on Aug. 31 st from wal-mart (money gram) and again was confirmed i needed to pay 3 paments to prevent foreclosure. I was also told to call back with the transaction number. So i made the payment ( amount told i needed to pay by Nationstar) and called back in the transaction code and was told all was good. On Sept. 15th i got a flyer in the mail wanting to buy my house before it was foreclosed on. I called the number on the flyer and asked where they got my address and was told in the newspaper for foreclosures. I immediatly called Nationstar and the agent said the money didn't post to my account but since i did get it on time he would fix it and not to worry and actually apologized for the mix up. He told me i was not in foreclosure. Well Oct. 7th Fanny Mae shows up to my house and says they on it. They said it was foreclosed on Oct. 5th. I paid what i was told mid August, Aug. 31 plus i talked to Nationstar on Sept 15th and was told everything was fine. If i would have been told i needed to pay more i would've. I talked to Nationstar on Oct. 8th and was told a manager will review it and they will get back to me on Oct. 12th about a possible rescind. If anybody has any advice PLEASE HELP. PLEASE SAY A PRAYER FOR ME THAT NATIONSTAR WILL DO THE RIGHT THING AND FIX THEIR ERROR.

email any help to : [protected]@msn.com

So what ended up happening?

scam

My mortgage was originally with Flagstar. I came back from a family vacation last year and my mortgage was sold to Nationstar. They told me that I did not have to make any mortgage payments for three months because they were trying to get me approved for Obama's new HAMP. I made my payments on time and Nationstar has sent my payments back stating that the payments were not enough to cover my debt which has acculumulated up to 34, 000. This company has been giving me the run around and I am facing foreclosure. I am looking into filing a class action lawsuit because all the money that I was paying into my mortgage has not been going towards it.

The complaint has been investigated and resolved to the customer’s satisfaction.

I just called Nationstar Mortgage for a payoff and it takes 24 hours via fax and there is a charge of $25.00. What a rip off! I spoke to a rep who was worthless. Bad way for a mortgage company to increase their profits

My home was heavily damaged by Hurricane Ike and is uninhabitable. I have no complaints or problems, whatsoever with the insurance company - Farmers Insurance. My agent was wonderful to me and responded quickly and was very concerned about my well being and my health. My adjuster was very nice and concerned about me, as well. They sent the adjustment check in a very timely manner and I endorsed and sent to my mortgage company as required by Nationstar Mortgage. I hired a contractor and he required 50% of the funds up front before he would begin the work. The total of the first draw ($19, 000 - half the adjustment) was sent by the mortgage company and the contractor insisted that I endorse the check over to him, which I did. It was almost one month before work ever started on my home. I got a new roof and rafter repairs. On the inside I had a small 1/2 wall removed, the kitchen was gutted, a small hall closet taken out to make room for a new bathroom vanity installation, flooring was laid in the area in front of the vanity, flooring laid in the kitchen and entry way (I provided all the materials for the floors), scraping of ceiling and re-texuring and painting of bedroom and closet doors in bedroom and insulation and sheetrock and paint installed in the kitchen and dining area (the room was also gutted by the contractor, of which he left all debris in my garage and back yard). The contractor's carpenter needed materials and I purchased them for him to continue the work, since the contractor would not return either his or my calls. Contractor finally called me back and told me he would leave me a check for reimbursement. The check he gave me was insufficient, which made me overdrawn in my bank and to exacerbate that problem, my bank charged me over $250 for insufficient funds. Things went downhill from there with my contractor, whom I suspect was having 'personal issues', and ultimately I had to fire him. The mortgage company sent someone out to my house to inspect the job and signed off at 45 percent completion. I hired a second contractor who jumped through all the hoops required by the mortgage company to release more funds so that the work could continue. The mortgage company kept coming back asking for additional documentation and finally the second contractor decided not to accept the job due to 'my mortgage company being too hard to deal with'. Finally, after many tears and sleepless nights, I found another contractor who was willing to help me. He agreed to repair my house with the remaining funds and has done everything the mortgage company has asked him to do and as of today, the mortgage company is refusing to release any more funds until the job is 100% complete. This is simply ludicrous. How can any company expect the job to be done with no money for supplies and materials, etc? It is like going to the grocery store and getting the groceries, but not paying for them until you have cooked and eaten them! Maybe a bad analogy, but nonetheless apt. This situation has caused me so much heartache, strife anxiety and thoughts of suicide. I am crying as I sit here and write this to you. I am living elsewhere and paying more expenses than I would have to if I was in my own home. Can you please tell me if I have any legal recourse or is this just the status quo for these greedy vulture mortgage companies who feed off of victims such as myself? I am hoping you might be able to offer some guidance to me. I am at a point of desperation right now. Any advice you can offer me is greatly appreciated. I simply don't know where to go from here.

Gmac sold our mortgage to Nationstar and everything was fine. Shortly after this transaction my husband lost his job...Nationstar contacted us about a loan modification. I would listen to my husband tell me the options of paying a note for three months that were about $500.00 a month lower than our regular note and if we did everything perfect they would refinance us at the new lower monthly note. I couldn't help but notice that we still recieved late notices although we did everything they told us now they are threatening foreclosure and my husband doesn't think it's anything to worry about. I am scared to death because our house is worth way more than we owe on it...HELP!

We are getting the run around as well. Being told to send a certain amount and they would start a repayment plan and when We did that they did not apply the money and are trying to foreclose. Also this happened once before and I sent a different amount they told me I needed to send and put it into unapplied funds and didn't apply it to my loan either. so it looks like I havn't made any payments when I have made several. They are rip offs and do not help you, but just lie and take your money.

I'm in the same situation with them. However my wife has great credit and she is not on the title. I'm thinking about just paying for things in cash from now on and renting an apartment with her credit rating and our combined income. F*&K um they can have the house. I'm 30k underwater on it anyway. We have no children so that's a plus I suppose.

Dear Ralph, pretty sure they're not supposed to charge you any money for modifying the loan..

Administrative Costs

Servicers may not charge the borrower to cover the administrative processing costs incurred in connection with a HAMP. The servicer must pay any actual out-of-pocket expenses such as any required notary fees, recordation fees, title costs, property valuation fees, credit report fees or other allowable and documented expenses. Fannie Mae will reimburse the servicer for allowable out-of-pocket expenses. Servicers will not be reimbursed for the cost of the credit report(s).

Cry some more, live within your means.

I am now very, very worried because I am also in this same situation! I have been waiting since January 20th 2010 for the docs that they said would be sent. I have spoken to Daisey Cortez on 01/20/2010, Ronda 01/21/2010, Tohara 02/3/2010, that's when I was told my case was rejected...what! I called again on 02/6/2010 spoke to James and he told me there was no foreclosure date. 02/9/2010 spoke to another james ext2119. called again 2/17/2010 james said that he still did not see a sale date, but i was getting letters from an attorney Macalla Raymer llc...I aqm sending pymts of $1364 cashiers checks. I still have no docs and I am told that they are behind with paperwork. I was given the modification dept tel# [protected] and spoke to Quinton, Asia( she was extremly rude) brian and broderick on 2/25/2010 he said I had an open case ( still no docs) finally I spoke to sheena and she faxed me some paperwork, that I filled out and faxed back with my paystubs. still no 'official docs" 3/9/2010 I GOT AN OFFICIAL NOTICE OF FORECLOSURE...I LOST IT. I spoke to joe and he told me that he does see that my docs have been imaged and he does not see a foreclosure date...I said to him has this attorney been told this. joe said that if a modification is done the foreclosure date is pushed back. i really don't know what to do now I am so scared. pls help.

I have the same problem My loan was sold to Nationstar from Flagstar in October 2009. I continue to receive late notices but I was told verbally that I am on a trial modification program, just send in $1599.03 by January 01, 2010. I sent the check December 20, 2009, The check never cleared my bank. I called on January 6, 2010 and was told by Renee that they returned my check because they need me to wire the money, send it quick collect or cashier's check. This was never told to me by the representative . The letter that came with the check said the funds are insufficient to cover the overdue amount on my account. I called back and they said dont worry about tht letter, just send the money quick collect. Yes I owe, but I dont feel comfortable sending money without proof it was sent. Should I be thankful that my check was sent back to me. My representative Jamie x3444 who said I was approved for trial payments will not return my calls. No one will give me anything in writing. I spoke with Chad on January 21, he was very rude, he said they dont have to send me any correspondance "I owe then money" .They will probably foreclose anyway. What to do?

I LIVE IN tN AND THANK nATIONSTAR IS RIPPING US OFF TOO AND WILL END UP WITH OUR HOME. wHO DO WE GO TO FOR SOME REAL HELP?

Mr. Cooper - over charges

This company does not work with any issue I bring up to them. They consistently have added fees and charge unnecessary fees for everything! They have a 15 dollar check processing fee. A 7.50 online payment fee and other ridiculous fees. I just finished a foreclosure proceeding and even though I did NOT get a Modification they still charged me late fees on...

Read full review of Mr. Cooper and 28 commentsBad Faith

I've seen enough other complaints on this site to repeat the same story. Suffice it to say, we have worked with them everyway possible for well over a year now and they keep delaying and otherwise displaying a total lack of good faith. All of this is on top of their overall inefficiency and rudeness. Is there a lawyer out there who is handling one or more of their cases. We are going to stop making payments to them and start paying a lawyer.

email us at - auroraloanservices dot cheats at yahoo dot com

Good luck to us all

The complaint has been investigated and resolved to the customer’s satisfaction.

This lender is terrible. We have been working with them for the past year. We have provided all the paper work they have requested and have been denied 3 times. They are threatening foreclosure if we aren't able to come up with the 30, 000. The representatives are rude, lack of customer services. I SWEAR, IF I COULD GET OUT OF THIS COMPANY I WOULD DO IT IN A HEART BEAT, I DON"T RECOMMEND THIS COMPANY TO ANYONE. IT SHOULD BE ILLEGAL FOR A LENDER TO PROVIDED FALSE INFORMATION AND DECEIVE THEIR BORROWS.

I cannot believe this crap that we are all taking. Both my husband and I have felt that our house is slowly being taken away. We to have been on program after program with no modification. We have been lied to. Our house has been in forclosure. This has been very hard to deal with stress wise. Right now we are in aspecial forbearance plan. We are going to have a lawyer try and do our mod this time. We have 3 months and if no mod then they told us we would have to come up with the $40, 000. How in the hell are we supposed to do that. They make me think of bad bad cuss words when I think about all of the crap that we have gone through. I am glad that someone is going after this Co. I wish myself luck because we are probably the next people being taken down by ALS.

ripoff

Beware Nationstar has a new way of ripping people off durring a remod.

they tell you that you qualify for the step 2 in a remod. to make sure you make the 3 payments and then send you a new set of documents and have you make 3 more payments. this will go on for 2 to 3 more times but in the meantime they give your loan to a company named Quality loans which forcloses on you. the bad thing about this is I made the payments to Nationstar like they told me to and I should have been talking to Quality Loans. Go check at the county recorders office. I thad to Learn this the hard way!

The complaint has been investigated and resolved to the customer’s satisfaction.

That's impossible. You start off on a trial plan to see if you qualify for a repayment plan. If you default on the repayment plan then you may not qualify for the next step which could eventually result in foreclosure.

Deceitful Company

Aurora Loan Services is a deceitful company that does not care about homeowners. After many months of applying for a loan modification so that I can keep my house, I finally received a call on 7/28/10 from an Aurora senior underwriter, Mike Lumpkin, stating that I had been approved for a permanent loan modification. He said, "Congratulations!" Oh, that was a happy day. He told me to sign the documents he would send to me and told me to make my first payment on 9/1/10. Well, the documents never arrived. Instead, he did an about-face and denied my modification on 8/27/10, and the foreclosure sale is set for 9/15/10. When I got home from a trip out of town, I discovered that Aurora had given me exactly one day to correct a title issue. One day! Who can fix a title problem in one day? Give me a break. Well, Aurora never gives anyone any breaks. So there goes my house. They can have it. It's way underwater anyhow. But does this really help the economy? They don't care at all about helping the economy or keeping a roof over a family's head.

The complaint has been investigated and resolved to the customer’s satisfaction.

Foreclosure

I am a victim of predatory lending practices. I bought my house in October 2003, and soon after Aurora Loan Services purchased my loan. A couple years later, I fell behind on my payments. Instead of working with me to lower my monthly payments, Aurora began charging me $200 more a month (to make up the difference from falling behind).

From [protected], I worked with them to lower my monthly payments again. After denying me several times, they finally agreed to work with me. They would charge me $1, 500 a month for two years and then my payments would go up to $1, 800 a month for the remainder of the 40-year loan. At that point, I had been living in my home for six years and I owed $10, 000 more on it than I originally bought it for. Making mortgage payments for six years had done nothing but put me into an upside down loan.

My husband lost his job in the fall of 2009 and we could no longer pay $1, 500 a month. Aurora refused to even talk to us about forbearance until my husband could find work. Instead, they immediately started the foreclosure process.

So long story short, our house is being foreclosed on. Aurora doesn't care about homeowners.

I did not realize how many people are being lied and cheated to by Aurora. I have tried every which way to work with them to save my home and have hit a wall each and every time! I have suffered serious setbacks from 2005 to present and have tried to retain my home regardless. I was expecting Aurora to work with me, however they have no intention of letting me keep my home unless it becomes a full out war. They took over 6 months to deny a modification and stated to me that the lender/investor was not interested in the Obama home save program. They did not at any time notify me of the denial, I became very concerned when I recieved the Auction date 9/22/10 and when I called them I got a recording saying to give them until November 20th to review. I finally got through to someone and they stated the denial letter was in the mail. I took them 6 months to deny me based on they don't do "2" modifications within 1 year. 6 MONTHS TO SAY THIS! I called for an amount to bring current and was told if I submit proof that I have the monies available (401K) they will stop the auction, however now that I amasking them for the dollar amount I'm getting a run around again! This is truly a nightmare! Get an Attorney these people are only out to rip off those unfortunates that seek their help. Homeowners BEWARE OF THE BIG BAD WOLF: AURORA, AURORA AND AURORA!

Kind of the same situation here, however I was denied a loan mod and Aurora kept stringing me along for over a year. I have done overwhelming research and have spoken with two seperate lawyers. Trust me when I say that foreclosure is a blessing in disguise. Im truly sorry to hear anyone who is struggling in these times and has had to deal with Aurora. I can afford my payments, however my home has lost almost 50% of its value, I have never been late on a payment and my Christmas present to myself this year is to start the foreclosure process. God Bless...!

yes I agree, we too have requested help from them to no avail, for them to consider a loan restructure, no go. Aurora are just a collection agency, I believe, so it's hopeless to even try to deal with them.

liars/cheats/crooks hamp not!

So glad to not be alone, yet I feel for others like us, having to work, deal with these people.

This first complaint is like many others.

Bought our home in march of 1999, we as lot of other americans do, we refinanced. After a few more years we refinanced again, and the last time was approx. 4 years ago, right before this economy took a crap.

Our loan is through fannie mae, yet the servicer at that time was flagstar. We had okay dealings with flagstar, which we had to. Like a lot of us, we had to file for the hardship program. We got accepted. Our monthly mortgage was before the hardship was $2, 048.30 (Ouch) we had sent in all of our letters, our check stubs, all that was needed. We got accepted, for this hardship.

We had spoke to a lady by the name of patricia l. Very friendly, and really wanted to work with us. She got our payment down to $683.00 per month for three months, then we had to do this all over again yet we had gotten approved for another modification with flagstar, basically another trial modification. We then filled out the paperwork and sent in all required papers to flagstar for the hamp program.

Okay, now, on the sixth payment, third payment of the second modification, flagstar sold our loan to what we call """"""""""""""""""""""""""""""""""""""""""""""""""""""the nightmare from hell mortgage company"""""""""""""""""""""""""""""""""""""""""""'""""""""""""""""""""""". """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""nationstar""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""".

Here now its time to pay our third installment of our second time around modification, and we receive a letter two days before its due saying they ""sold"" our loan to nationstar... Having nothing but this paper saying we sold your loan to this company..

No account number, no address, not even a phone number. We look them up on the internet, find this nationstar, and they have no information on us and no information to give to us. We call flagstar, they tell us; we have sold your loan, and you no longer have the account with us, and to contact nationstar to find out where to send payment... (Oops) payment is now late and we are now in default... Finally, after a few months, yes a few months, we finally know where to send the money to, but its not the $683.00 its the full amount along with the months, we are now behind...

At this time, the economy, is really in the crapper, and im not working, my husbands business has slowed down to a minimum and we are barely making ends meet. We cut back on everything, food, lights, clothes, gas, electricity, etc. We're living sometimes off the means of our friends and family. (Thank you to dave and karen wiley, mr. Steven hallsted and the others we were able to pay back)

At this point, ive given up, thrown my arms up and said f*** it all... So my poor husband now is in charge of everything, bills, dealing with nationstar, working and trying to provide for his family...

One day I over heard him talking to nationstar (Chad) omg-ness this boy/man/rude person on the other end couldn't be from our mortgage company. Well, it was. He was yelling and cursing at my husband putting him on speaker, then cracking jokes, like are you on drugs mr. B. Finally after chad hung up on my husband, thats when I decided I would take over the mortgage company. Not to say I was going to find someone nicer, or I would even be nicer, yet I needed to give my husband a break from the insanity of nationstar.

On july 1st of this year, I took over. I have recordings of all I have spoke to, I have recordings of them after they ask me all the pertinent information, I ask for their name, they hang up on me. I have all the dates, times, and how long these conversations or lack of conversations lasted. Either ive recorded them or ive written it down, down to the seconds on the phone with them...

Its now august 24, 2010 and now our dealing are with a lady/girl named chizo (chizbo) ~ loss mitigation rep~. Some of their names I felt as though I was going into a cartoon. One I talked to was named: pinkie, oo'kay whatever...

Three days ago she wanted us to send her $2, 048.30 and keep the money they had gotten from flagstar $1, 376.70

No modification, chizo and I had gotten into a bit of a tado and I said I was going to call back. I called back around 2pm central, so about 5 minutes into a conversation I was put on hold by justin, and chizo got on the line. This was not looking good. She proceeded to tell me to hang up and call back, as she wasnt going to discuss my file due to she didnt have it on the screen. My replay " this is me calling back, I didnt ask to speak to you, just put me on hold and I will wait. Brian the manager of these reps. Supposedly got on and looked at my file and said our hamp had been denied. Really? And what time did this happen, I asked, brian replied, at 2:17pm central. The next thing out of my mouth was, uhmmm what a conundrum I just got put on hold with chizo at 2:14pm and mow my hamp had been denied? Chizo, whatever she did, she did wonders, he replied... Yes, she sure did, my response to him...

So now, our home is going up for auction on the 16th of september, 2010 at 9:30am

Chizo called today and told my husband we had to pay by the 26th of august $4, 098.60 and we have no idea if we will get qualified, if not we just gambled our money away...

These people here at this company, have lied to us.

1st lie made by chad: we never received any type of paperwork, yet we have the fax sheet that says he received it all 31 pages

2nd lie made by chad: telling us to send him $683.00 for what, we're still unsure. Maybe he wanted us to pay his back child support, naw, now we know.

3rd lie made by chizo: I really want to work with you to safe your home

4th lie made by chizo: we need a contractual payment of $2, 048.30 by the 26th of august, (Which) this lie runs into the lie that was today.

5th lie made by chizo: we need $4, 098.60 by the 26th of august, 2010

So my friends, this has been our story dealing with ==============nationstar mortgage===========

The long and short of it, they don't want to work with you. They will take your money and the free government money and deny, deny and deny! Just waiting for housing prices to go up. We are the tenants, and caretakers of our homes, yet their not paying us to take care of them...

Did you know this: the hamp program has only qualified 31% of the people.

The government set aside 50 billion dollars, yet has only used 1.5 billion in a year and a half

For one, the banks don't want to do the paperwork, they take the money and collect interest on it, you know the free money the government has given them

Second: people are paying off their mortgages that aren't worth the value of their home. Ex: they are depleting their 401k's (If they have one) , borrowing money (If someone has the money to loan them. )

Americans need to take a stand, call your congressman, write them letters, do whatever it takes to make them listen. Don't make any deals unless you know exactly what your getting. Take that last stand, don't do upgrades to your home, thinking your going to get approved, cause the looongg and short, the chance of you being that 31% who get approved, is slim to none. Good luck!

As for nationstar, you can take our home, and make it yours... We survived without you for years, and we will survive without you again. Karma, is a bit** so to all those folks that we spoke to at nationstar, remember us in your dreams, because when its your time, you will be judged by the one and only!

R. And p. Blakeley

You know us!

God bless you and your family, may you reap in the sorrow you have caused so many!

I am another victim of this pack of liars. We have filed a complaint with our attorney general here in Oregon against this company. It won't save our home, but I sure want other potential victims to know who these groups of sewer dwellers are. We are now dealing with the lawyer from the eviction side of this tragedy. I have written up our experience under Nationstar Mortage Hamp Mishandling.

1st of many on this company

So glad to not be alone, yet I feel for others like us, having to work, deal with these people.

This first complaint is like many others.

Bought our home in March of 1999, we as lot of other Americans do, we refinanced. After a few more years we refinanced again, and the last time was approx. 4 years ago, right before this economy took a crap.

Our loan is through Fannie Mae, yet the servicer at that time was Flagstar.We had okay dealings with Flagstar, which we had to. Like a lot of us, we had to file for the Hardship Program. We got accepted. Our monthly mortgage was before the hardship was $2, 048.30 (OUCH) We had sent in all of our letters, our check stubs, all that was needed. We got accepted, for this hardship.

We had spoke to a lady by the name of Patricia L. very friendly, and really wanted to work with us. She got our payment down to $683.00 per month for three months, then we had to do this all over again yet we had gotten approved for another modification with Flagstar, basically another trial modification. We then filled out the paperwork and sent in all required papers to Flagstar for the Hamp program.

Okay, NOW, on the sixth payment, third payment of the second modification, Flagstar SOLD our loan to what we call """"""""""""""""""""""""""""""""""""""""""""""""""""""THE NIGHTMARE from HELL mortgage Company"""""""""""""""""""""""""""""""""""""""""""'""""""""""""""""""""""". """""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""NATIONSTAR""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""".

here now its time to pay our third installment of our second time around modification, and we receive a letter two days before its due saying they ""SOLD"" our loan to Nationstar... Having nothing but this paper saying we sold your loan to this Company..

NO account number, NO address, NOT even a phone number. We look them up on the internet, find this Nationstar, and they have NO information on us and NO information to give to us. We call Flagstar, they tell us; we have sold your loan, and you no longer have the account with us, and to contact Nationstar to find out where to send payment... (OOPS) payment is now late and we are now in default... Finally, after a few months, YES a FEW Months, we finally know where to send the money to, but its not the $683.00 its the full amount along with the months, we are now behind...

At this time, the ECONOMY, is really in the crapper, and Im not working, my husbands business has slowed down to a minimum and we are barely making ends meet. We cut back on everything, food, lights, clothes, gas, electricity, ETC. We're living sometimes off the means of our friends and family. (Thank you to Dave and Karen Wiley, Mr. Steven Hallsted and the others we were able to pay back)

At this point, Ive given up, thrown my arms up and said F*** it all... So my poor husband now is in charge of everything, bills, dealing with Nationstar, working and trying to provide for his family...

One day I over heard him talking to Nationstar (Chad) OMG-ness this boy/man/rude person on the other end couldn't be from our mortgage company. Well, it was. He was yelling and cursing at my husband putting him on speaker, then cracking jokes, like Are you on drugs Mr. B. finally after Chad hung up on my husband, thats when I decided I would take over the mortgage company. Not to say I was going to find someone nicer, or I would even be nicer, yet I needed to give my husband a break from the insanity of Nationstar.

On July 1st of this year, I took over. I have recordings of all I have spoke to, I have recordings of them after they ask me all the Pertinent Information, I ask for their name, they hang up on me. I have all the Dates, times, and how long these conversations or lack of conversations lasted. Either Ive recorded them or Ive written it down, down to the seconds on the phone with them...

Its now August 24, 2010 and now our dealing are with a lady/girl named Chizo ( Chizbo )~ LOSS MITIGATION REP~ . Some of their names I felt as though I was going into a cartoon. One I talked to was named: Pinkie, OO'kay whatever...

Three days ago she wanted us to send her $2, 048.30 and keep the money they had gotten from Flagstar $1, 376.70

No Modification, Chizo and I had gotten into a bit of a tado and I said I was going to call back. I called back around 2pm central, so about 5 minutes into a conversation I was put on hold by Justin, and Chizo got on the line. This was not looking good. she proceeded to tell me to hang up and call back, as she wasnt going to discuss my file due to she didnt have it on the screen. my replay " this is me calling back, I didnt ask to speak to you, just put me on hold and I will wait. Brian the Manager of these reps. supposedly got on and looked at my file and said our HAMP had been denied. REALLY? and what time did this happen, I asked, Brian replied, at 2:17pm Central. The next thing out of my mouth was, Uhmmm what a conundrum I just got put on hold with Chizo at 2:14pm and mow my HAMP had been denied? Chizo, whatever she did, she did wonders, he replied... Yes, she sure did, my response to him...

So now, our home is going up for auction on the 16th of September, 2010 at 9:30am

Chizo called today and told my husband we had to pay by the 26th of August $4, 098.60 and we have NO idea if we will get qualified, if not we just gambled our money away...

These people here at this Company, have lied to us.

1st lie made by Chad: We never received any type of paperwork, yet we have the fax sheet that says he received it all 31 pages

2nd lie made by Chad: telling us to send him $683.00 for what, we're still unsure. maybe he wanted us to pay his back child support, naw, now we know.

3rd lie made by Chizo: I really want to work with you to safe your home

4th lie made by Chizo: we need a contractual payment of $2, 048.30 by the 26th of August, (which) this lie runs into the lie that was today.

5th lie made by Chizo: We need $4, 098.60 by the 26th of August, 2010

So my friends, this has been OUR story dealing with ==============NATIONSTAR MORTGAGE===========

THE LONG AND SHORT OF IT, THEY DON'T WANT TO WORK WITH YOU. They will take your money and the Free Government money and DENY, DENY and DENY! Just waiting for housing prices to go up. we are the tenants, and caretakers of our homes, yet their not paying us to take care of them...

Did you know this: The HAMP program has only qualified 31% of the people.

The Government set aside 50 billion dollars, yet has only used 1.5 billion in a year and a half

For one, the banks don't want to do the paperwork, they take the money and collect interest on it, you know the FREE money the government has given them

Second: People are paying off their mortgages that aren't worth the value of their home. Ex: they are depleting their 401k's (if they have one), borrowing money (if someone has the money to loan them.)

Americans need to take a stand, call your congressman, write them letters, do whatever it takes to make them listen. Don't make any deals unless you know exactly what your getting. Take that last Stand, don't do upgrades to your home, thinking your going to get approved, cause the LOOONGG and short, the chance of you being that 31% who get approved, is slim to none. Good luck!

AS FOR NATIONSTAR, YOU CAN TAKE OUR HOME, AND MAKE IT YOURS... WE SURVIVED WITHOUT YOU FOR YEARS, AND WE WILL SURVIVE WITHOUT YOU AGAIN. Karma, is a Bit** so to all those folks that we spoke to at Nationstar, remember us in your dreams, because when its your time, you will be judged by the one and ONLY!

R. and P. Blakeley

You know us!

God Bless you and your family, may you reap in the sorrow you have caused so many!

a sign of hope for others

I had good experience with nationstar and think they are ethical. My modification became permanent this week - what a blessing! Saves me $600. Per month and I can now stay in my house. It took a very long time to process, almost a year counting application process and trial period.

I had flagstar mortgage for my home loan. They sold my loan to nationstar the same year I applied for the "make homes affordable modification program" and I had to do paperwork all over again.

The waiting on fannie mae to sign final papers took couple of months. Nationstar has two different departments for regular loans and modification program and they don't communicate very well with each other, so I would get many recorded phone calls from the regular loan dept. Telling me my pymt was late, but every time I called to verify there were no problems the representatives were very nice and knew what they were talking about, and would reasssure me that things were going okay and to ignore the calls from the other dept. I felt they tried hard to get me into the program, and they followed up with whatever the gov't needed very quickly.

I'm writing because I had read alot of complaints and got very worried a few months ago, thinking I might be getting screwed.

The complaint has been investigated and resolved to the customer’s satisfaction.

Yeah, mine was great at first too. Wait till you start getting all the legal fees and such related to your mod.

Sandra, this is the first positive note on the internet I have seen about Nationstar and only hope it is in fact true. My load was also sold from Flagstar and everything else is similar to what you experienced but I am still waiting on the permanent loan modification. If it happens, I will be able to live my life again. If they screw me, I will be contacting an attorney and hope they can sort it out. I have done nothing wrong but gotten a reduction in my salary that made my payments very difficult to make but I sacrificed everything to never miss a payment. I have yet to miss a payment but their chronic phone calls might suggest otherwise. Thanks for writing, I hope your message isn't a prank.

HORRIBLE

I have tried for the last 2 years to remodify my loan with this company. They always take 4-6 months and then send me declination letter. Each reason for the decline is different. All they want to do is trial basis for 3 months but then they NEVER actually remodify my loan. This company is truly a rip off. They have forced me into forclosure and I am losing my home. No other choice.

The complaint has been investigated and resolved to the customer’s satisfaction.

This whole mortgage situation is a nightmare, I don't know what state most of these folks are from but as far as I know and believe me I have contacted every possible entity to tell them how these loan companies work. they only "service" the loans and they do a really crappy job of it. There "agents" are unprofessional, incompetent and if you send an email don't expect an answer. I think that the best way to draw attention is for mass complaints to be sent/faxed to the federal trade commision. Make the lenders produce original loan documents. without those how can they prove that anybody owns the loan! they have been sold out from underneath us so many times, it's sickening! forclosure in MN takes 10-15 months, when they come to kick you out ask for those documents and stand your ground. I know that in congress Elizabeth ? is working on a consumer complaint board but I don't know how that will impact us current home owners. mass complaints about the companies is the only way. I respectfully say that if we struggle to make our payments in the screwed up economy Mr. Bush left than how can we afford to march on washington?! believe me I dream about picketing. Blessings to all you hard working folks, keep your heads up and remember you are not alone. How can we all get together to change this?

wrongly forced placed insurance

My nightmare began in December 2009. Here is a summary of what has been going on:

November 15th 2009 I received a letter stating that State Farm was not going to renew my homeowners insurance, that I have had with them since 2003 and as of December 18th 2009 my insurance with them would be cancelled. Due to claims turned in due to several damages a tree limbs had cause to my roof over the last two years.

On November 30th 2009 I spoke with Justin at Allstate and started my house insurance with them. I was told that as of that day 11/30/2009 I was insured with Allstate and did receive a email showing I was insured as of that day. Justin said he would fax NationStar the information they needed showing I was insured with them.

At this point I was insured twice, since State Farm was not going to cancel my policy until 12/18/2009.

So on December 1st 2009 I called State Farm (which had already been paid for the month of December) and cancelled my insurance with them since I did not need to be insured twice. I did even receive a small refund later from them since I did have the coverage the full month.

Sometime around the first week of December 2009, I received a letter from NationStar stating that I had received a letter from State Farm that I was no longer going to insured with them as of 12/18/2009 and that if I was not insured by that time they would have to force place insurance on my home. Immediately called Justin my Allstate agent and told him. He assured me that he had faxed them the information needed to Nationstar on 11/30/2009 that day my coveage started and would re-fax said information.

I also called NationStar and spoke to one of the operators (as that is all you get) and explained to them that the house was in fact insured with Allstate as of 11/30/2009, gave the policy number and the phone number and Justin’s name. I was told that this would take care of the problem.

Several weeks later I received a letter from NationStar stating that they were force placing insurance on my home. I was very upset. I could not understand why this was happening. How could they be placing insurance on a home that was already fully insured. I once again called Justin my Allstate agent told him what I had received. He said he was going to fax and call NationStar to inform them that I was insured as of 11/30/2009 and give them the information (once again) that was needed.

In my statement after that my account was placed into escrow due to non-insurance on the house and the house now had homeowners insurance force placed by NationStar. When I was fully insured and there had never been a laspe.

Since December, 2009 until March, 2010 I have called (spoke with different people each time) no less then 6 times and so has Justin my Allstate agent, giving NationStar the information needed proving I had been insured and that there was NO lapse in my insurance what so ever. And that forced placed insurance should have never been placed.

In April, 2010 I spoke to someone at NationStar after still receiving statement showing I was still insured twice, once through NationStar and then with the insurance company that was forced place on my home.

This individual assured me that the matter was taken care of. This was direct from the insurance company which force placed insurance on the house. Once again, on that day my Allstate insurance agent spoke with the same person I did, assuring them that I had insurance with Allstate as November 30, 2009. And once again I thought everything was fine.

But since then I received my statement and I am still being charged for insurance that has been force placed. I have sent several letters to NationStar, with copies of my Allstate policy showing I was insured with them as of 11/30/2009 and have called several times.

My Allstate agent Justin, has called and faxed information to Nationstar showing we were insured with them since then and there was NO lapse in my insure. I have even mailed a copy from StateFarm showing I cancelled insurance with them only after being fully insured with Allstate.

On April 30th, 2010 I received a letter from a Eliot Robinson, Customer Care Specialist, from Nationstar, stating they their records indicate that Nationstar has received prooper evidence showing that there was no lapse in our insurance. And that they have taken their lender placed insurance off the account and add Allstate.

But as of July 16, 2010 this has NOT been done and I am still being charged for cost I should have NEVER been charged for. And since that letter in April, 2010, I have mailed and called as well as Allstate in regards to this matter but it is still not being taken care of.

On July 16, 2010 I spoke with a gentlemen that was very nice, I explained to him the problem, he then transferred me to someone in the escrow department that he felt would be able to fully take care of the matter for me.

I am not sure who that person was, as she would not give me her name. She was very rude and not helpful at all. She in piled that the amount I was wrongly charged for by them forcing insurance on my home would be up to me to pay. And then said she was not going to talk to me about this matter any more and hung up. I was not rude nor nasty to her.

An as of today 7/17/2010 I am told I am only sending in particle payments and that I am behind for the last two month. Which is not true. I have been sending in my 677.00 each month like always...NEVER missing a payment nor late since having the mortgage. But because of the forced placed insurance that should not have been placed in the first place, they are showing my to be behind.

As of today, July 19, 2010 the hell is still going on. I may have to hire an attorney to finally get this straghtened out.

My advise to you, save everything, record calls if you can, mail letters that have to be signed for, do what ever you can so if you have to go to court, you are prepared. This company is crooked and they are not going to give in.

Seriously. Get a lawyer. Nationstar is the worst and the only way to make them deal with you fairly is to force them. RESPA is on your side, get a a competent attorney, one who will also look into the county assignments for your property. You should look to see if you have any missing assignments because if you do, you have a broken chain of title. Ask your attorney about "clouded title" and "broken chain of title". Nationstar may even be illegally collecting payments from you. Get an attorney asap.

I have had basically the same problem. In July 2011 right before NationStar bought First Horizon, First Horizon put forced placed insurance on our home, thus opening an escrow with a negative balance. NationStar buys them out, we know nothing about the forced place insurance or the negative escrow, NationStar pays our purchased insurance along with us paying it (Farm Bureau) and our insurance keeps returning their checks - again without us knowing anything about it. Until August of this year when NationStar pays Farm Bureau BEFORE we do and send our already negative escrow even further backwards. On our request the last check was returned to NationStar.

Ends up...I send NationStar all the info they requested including Insurance info back to January 2011 showing our policy never lapsed or canceled, that would open a 'escrow analysis review', they could find out Who did forced placement and NationStar would be refunded by them - it was not our problem but instead between NationStar and the forced placed insurance company.

Well, it's October...the 'escrow analysis review' found that our escrow was in the negative when NationStar purchased it and the money had to be repaid - our mortgage payment is on the line, as is our credit standing if we hold out and refuse to pay escrow.

It's ridiculous! What is the recourse? We are talking about right at $700, too much for us to let them get away with but what are our options? They are crooked! Any suggestions?

What you want to do is send them a FED EX envelope with your Allstate Declaration Page showing that you have always had coverage and request a signature and receipt of that mailing. Upon receiving confirmation of the receipt of the mailing, immediately call the bank and demand that all charges be removed from your account and your account be restored to good standing. If you don't get anywhere with that, you may have to consult legal services. Don't let this go! Your credit rating depends on it!

fix it nationstar or lawsuit

Gmac sold my mortgage too, to nationstar in december 2008. Since then my life has been hell! I didnt even get notification that they had bought my loan until almost march 2009. I have been on the phone with someone for hours of my life that I will never get back. They did not have my correct address or name. I, like others, have struggled since the beginning with the issue of escrow insurance. They said I had a lapse in coverage when I was with gmac which was untrue and had provided the information to prove it from gmac and my insurance company to no avail. I am sitting here now looking for every address I can find to mail a packet demanding action or I will be finding an attorney in 30 days! I have paid every payment but do to their incompentance I have been forced to pay certified signed reciept every month!

Someone has to stop this company from harrasing paying people any further!

I am mailing my packets today and then lawsuit

Stephanie morris

[protected]@leeu. Edu

The complaint has been investigated and resolved to the customer’s satisfaction.

liars/cheats/crooks

To anyone who is having issues with Nationstar Mortgage or by the above DBA-Names above, please contact me. I'm sure all of our stories are the same. This company is BAD. I've got my State Congressman and his office involved. I've got Nationstar Department Head's email addresses/phone numbers and all contact info. I have advice to all of you on what to do. Draft letters and send them. We are fighting them and won't give up.

1 year and 2 months now we have been in modification hell. Flagstar sold us out in our last month of the trial. Its been almost one year with Nationstar, then they pulled the usual...no paperwork, no this, no that, etc. and then came the foreclosure notice...that was a few weeks ago. The story is changing now, since I've sent out the letters and got my congressman involved, now Nationstar is calling us! Yes, we actually have a Rep, with a real phone number and a real email address! Amazing, I know. But what we did seemed to work. I would like to try and help all of you.

I have too much info to tell you in this board's format, so please email me if you would like my "free" advice on what we are doing. Perhaps if we all do the same thing they won't get away with it.

We've actually seen some movement in our dealings with them since I contacted some State Reps and Head's of Fannie Mae. We'll wait and see, of course, it can change overnight with Nationstar. However, I do think that I've got some tactics that may help some of you. You also need to send Nationstar a QWR letter. Be careful though, it needs to be worded CORRECT or they don't have to respond to it. There are some key words you need to include in order for it to legally stand up in court. You also send a CC to everyone on my list of names. I'll give you all copies of what I have and you can fill in your name/etc. and send out your own.

It's a start, and it does get their attention. Let's GANG UP ON THESE JERKS! Stand up and fight people! Or they WILL Take your home.

Next steps to follow...via email.

my email is: [protected]@techie.com

Feel free to contact me if you like. - don't worry, i'm not a weirdo and I'm not selling anything. I'm just sick of Nationstar's crap and I need more support to fight them.

Not Going Down In Oregon!

Well "Taking control" I see you've been active on the board posting comments after various complaint posts. For starters, it costs money to start a lawsuit, at the very least it takes time. Most of which any of us have at the present time! Remember? We are in foreclosure or close to being in foreclosure. If any of us had the money to plop down as a retainer on a attorney we would probably be using it to get current on our mortgages or hire an attorney to file bankruptcy. Furthermore, your case sounds like a 1 in a million chance drawing! A mortgage company or servicer rarely looses a mortgage, let alone the investor or investors! So, good luck to you on your lawsuit. You should have no problem with it since you are apparently VERY lucky to begin with.

Thanks

UPDATE TO ORIGINAL POST

We got our mod offer as of two days ago. Nationstar actually called us with the offer. Gee? I wonder why? hahahaha - I guess all the letters we wrote and people we contacted about their treatment to us worked!

The offer is good for 30 days and now we are in the negotiation stages. The mod actually looks good. Interest rate drop for 5 years, down to 2%, with 1% increase every year and a cap at 4% at 5% for the life of the loan. Just waiting to see what fees/charges/amounts they will be tacking on. Thats where the negotiation starts and that's where keeping every piece of correspondence with them comes in. Wish us luck!

We lost our home to nationstar in 2015, every month they screw with my credit report. they took our house, sold in in june 2015 and reported today, that the account is open again, (5th time in the last 9 months) saying I some how made a 300 payment and missed dec 2018 payment and owe over 25, 000 to them. a. why would I make a payment on a home I haven't owned since 2015, and the account has been closed with 0 balance, now showing over 25, 000 owed. when I disputed it with experian, I was told by nationstar to drop my dispute or they wouldn't fix anything, then I was told "they don't report to the credit agencies, that the credit agencies are the ones changing the reports ([censored]) I have also been told if I keep disputing things on my report about them, they would change my credit as often as they like, so it never comes off my credit report. this is [censored], and its stressing me out in a bad way. they also claim we missed 22 payments from [protected], to which I sent them the cashed checks from our bank, they said we were foreclosed on, yet we never went to court, we did a deed in lieu (which they lost) they said we did a loan modification, which we did not, we refused to do one, and that's when the crap started with them. they will not furnish us with these so called modification papers, (I would assume because they are forged with our signatures) we paid the taxes on the house after it was sold since they reported we made money off their sale (which we never saw any money) yet they say they foreclosed... someone needs to stop these people!

I recently had my mortgage transferred over to "Mr Cooper" AKA Nationstar and transferred $50, 000 from my credit union to them. The amount shows as being reflected in the Mr Cooper account but also shows a 50k balance in my credit union account which I think is strange. This may just be a technical error, but I want to protect myself.

I make payments online through my banking institution, but Nation Star doesn't post the correct/entire amount. I keep being charged late fees though I'm paying on time, and my payment amount keeps fluctuating (up and down) and then the rest of my payments used towards the fees they continue to charge me. Smh

Nationstar is a loan server they only service the loan for investors who own the loan that's why if they can keep you from making your payments on time or lose them then they can start charging fees by law to make your life miserable and force you to go in default only to steal your equity and your home. Get a local mortgage company and get new loan or you will be in trouble all the time with this company. I know because I had a home I owed $80, 000 on loan and it was worth $165, 000 and Nationstar would not help me to save it. No modification help which took a year to drag it as long as they can to collect inspection fees, phone call fees, late fees and forclosure cost and on and on till you have no equity you can get out of your home it. They are crooks that's how they make money stealing it from you.

cant never get an answer, terrible company stay away from.

I am soooooo. Sick and tired of you messing up my account. You have been the WORST mortgage company I have ever had.

They are liars denied me for a home mod stating i didnt turn in all paperwork was aclear lie and they mske up numbers stating im behind in my payments i think trying to scare me its bothering me physically and emotionally

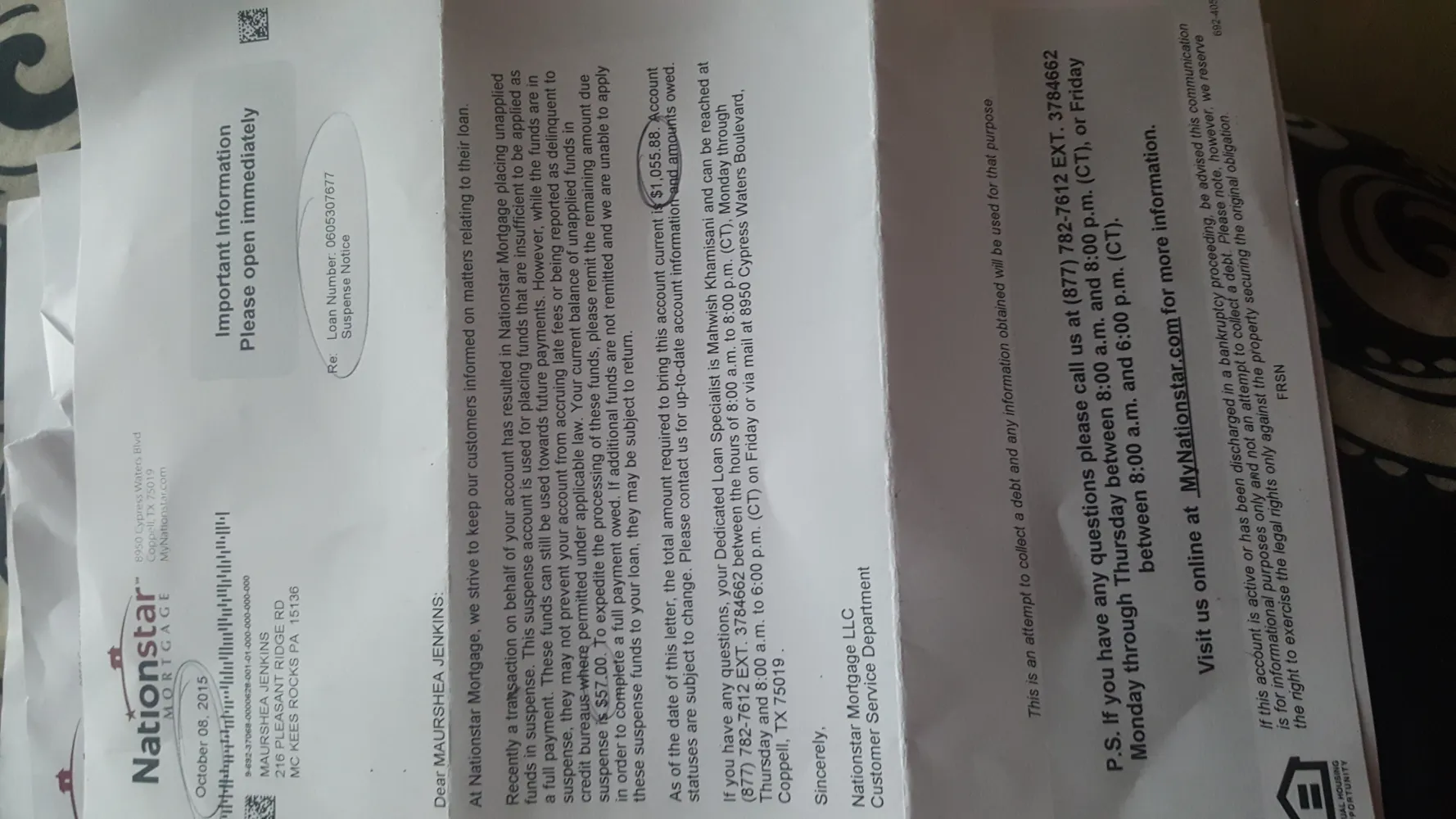

Ever since 2013 when they implemented dedicated specialists they have not kept record keeping at all. They don't apply payments, return payments, hold extra monies as "suspense" accounts. Just Plain Crooks. I

Monthly repeated phone calls to remind us to pay our mortgage before it is due.4e65f

I'm sure this is all a misunderstanding and will eventually be resolved. Good luck to all.

A word to the wise: Don't post here if you think you might change your mind. Management does not allow for deletions of posts or accounts. Just a thought.

harassement

My name is michael adum, in may 2001 I bought my house in houston and my morgage company (Principal residential morgage) sold the debt to countrywide two years after, then I refinanced at same interest rate (7, 50%) but without the scrow, because I preffer pay it by myself, everthing was ok. But this company said I paid my school taxes on 2009 late. (Feb 5 2010) when it should be paid on or before jan 31, 2010. I sent this company a letter from the school tax collector telling them I never been delinquent but this people don ' t accept the letter, now they sent me a letter telling me I have not insurance, but I have it, and they have the information from my insurance company but they want to put me an insurance in my house, finnally what they want is, rise my morgage payment puting the scrow. I never been late in my morgage, taxes, insurance, and, besides because my age, 67 years old have a payment arrangement in my school taxes to pay it in quaterly installments, (Never late) , but no one of the almost twelve people I did talk in this company (Always answer a different person never the same I talked before) can do nothing as they said. This situation is bringing me sick i'm stressed and my wife too I have proof of this kind of harassemeent against an old person from this people. What can I do?

My mortgage was turned over to Nation Star this year and I have had nothing but problems ever since. I have faithfully submitted my payments every month, never late. They claim they are not receiving them and charging me late fees. The burden of proof is on me. I am spending so much of my time. The word frustrated does not even come close to how I feel. I call, send emails, fax and no one has made any contact with me. I am tired of talking and complaining. I want to really do something about this company. If what everyone lists on this site is true then we need to take it to the next level and file a class action suit. A company like this should not be able to push people around. What do I need to do? Who can I contact? Who will be their next victim?

loan mod

One when first getting the loan 11 yrs, I asked to have the realestate taxes and insurance in the monthly payment.

This was not done.

Two they would not put me on the loan, but however they took a cert bank ck from me.

Although we had ruff times and sometimes fell back on payments, I struggled to keep a float.

In sept I applied for a home mod and was told that the payments were to be 589 month, after the sept payment of 774. They request info and I faxed over several times and paid $ 35 I continously keep in contact with them, then in dec they told me we had to do the process over again. They did not resubmit it until feb then they call on may31, 2010 telling me they did not approve it and now we owe 8, 0000 and some odd dollars, and we need to pay

Now. Now we are faced with losing our home. How is this fair. Please anyone who can help please, I have 3 disable children

The complaint has been investigated and resolved to the customer’s satisfaction.

shady business practices

Last year, Flagstar sold my mortgage to NationStar. I had always made timely payments with Flagstar and I have excellent credit. Once NationStar got my mortgage, however, they immediately starting treating me like a deadbeat. They would call and harass me monthly about my payments--before the due date--and tell me to pay up immediately. They asked me for personal information but, since I couldn't verify they were who they said they were, I refused to give the information to them. When I sent my timely payments, they would hold the payments for several weeks--until it was past the due date. Then, they would cash the checks and charge me a late fee. While they were holding my check and pretending not to have it, they would call and call and call me. (I sent the checks directly through my online banking, so I could verify the date they were sent, so I know they had to have it.) Once, when I was on vacation and not answering my cell phone, they called non-stop, so I put a block on their number so it wouldn't ring through any more. The only way I was able to stop the harassment was to scrape together enough money to make two mortgage payments in one month, sent a few weeks apart. Now, since I pay them a month in advance, the harassment has stopped. However, most people can't do this and no one should have to go through that kind of treatment.

My next issue with NationStar is trying to refinance through the government's Make Home Affordable program. Supposedly I qualify, but they would not refinance my house despite my having enough income and excellent credit. Instead, after refusing to help me refinance, they sent me a letter "certifying" that I had "withdrawn" my loan request. I couldn't believe it! They aren't being honest about their refusal to participate in the government program.

The latest problem is with my homeowner's insurance. Flagstar had always paid my homeowner's insurance out of escrow in a timely manner. However, today my insurance company called to tell me that they had called Nationstar about my late payment (it was due on the 15th) and Nationstar had told them that I didn't have an escrow account with them, so that I needed to pay the insurance company directly. The insurance company told me that I need to pay them the year's amount immediately or they would cancel my insurance. I told them that NationStar is required to pay it from my escrow account, so I would call them about it. NationStar at first told me that my "condo association" paid my homeowner's insurance. I told them that this was false, that they were supposed to pay it as Flagstar had. Then they tried to tell me that I didn't have an escrow account with them because Flagstar hadn't told them about it. I pointed out that Nationstar had raised my mortgage payments last year because of an "escrow shortage, " so that this was blatantly false. I also pointed out that there were complaints all over the Internet about them doing this sort of thing to other people. I demanded that they pay my homeowner's insurance immediately. And, lo and behold, Nationstar was suddenly able to look up exactly who they should be paying and how much! Nationstar said that they would do "research" into the problem today and then "overnight" a check to the insurance company. I asked when they could expect to receive the check, since they were going to cancel my insurance soon. I finally got them to promise "next Tuesday at the latest." I also insisted that they write me a letter apologizing for their mistake and agreeing to pay my homeowner's insurance in a timely manner in the future. We shall see whether these things happen as promised. I have little faith in this company. They are unethical.

@NateP: I have since found out that Nationstar's harassing phone calls are an FCC violation. If they are still doing this to you, report them to the FCC. Also, start keeping a log of the calls.

I realize your post was last year, however, the same story is happening to me. I have the reoccurring payment set up, yet they call and call and... never leaving a message, caller id did not identify them and when I did answer the phone no one was on the other end. I called the number back, and find out it was Nation Star, I asked them why they keep calling, they say they are calling about a payment; however, I have a reoccurring payment set-up. Then they start with treating me as if I am a dead beat. There should be something out there preventing companies from buying your mortgage without your knowledge or consent. This company is horrible and the service is twice as bad.

Our loan was sold from First Horizon to Nationstar and we were notified only one month in advance of this happening. We are having similiar issues. We have a Grace Period in which to make our payment. We are always on time, but have had to make some payments within the Grace Period depending on when our paychecks are received. As soon as the 3rd of the month rolled around this month they started calling our home daily. I contacted them and told them that our payment would be made within the Grace Period and to stop calling our home. They continued to do so and one rep got particulary nasty. I have sent them a certified letter telling them to stop calling our home or I would report them to the FCC. So we shall see what happens. In the meantime I am exploring how to put a block on my phone from receiving any future calls from them. Despicable company!

I am being harrassed regularly by this company. I get robocalls on a regular basis and their reps are constantly asking me "when can you get that payment in?" in a sneering, annoying tone when I call them to ask to be taken off the robocall list.

Citi sold my mortgage to them a couple of months ago. My payment was set up automatically from the origination of the mortgage in early 2008, comes out the same day each month (on-time), and has so for the entire time I have owned the homw. I have never been late on any mortgage payment, and have never defaulted on anything in my life. My payment history is flawless and my credit is excellent.

I believe what Nationstar is doing is probably against the law, and I have some friends in the class action lawsuit business who are always looking for corporate crooks like these. You'd be surprised to learn how many companies are built entirely on unethical and illegal practices. Many times it's worth the risk to companies like Nationstar because the cost for an individual plaintiff to hold them accountable exceeds the recovery, but when you consolidate a few hundred or few thousand plaintiffs, you've got the power to put them out of business.

Anyone who makes progress reporting the company, getting them to cease their harrassment, etc., please post your results here.

Where does one report them to the FCC (can it be done online)?

I have had these exact same problems with Nationstar! It sounds like my life story.

The only difference being that they would call my place of work to collect payment. They have my cell number, yet they never call that, in the rare event that they do, they never leave a message. They have no problems leaving messages at work though, they would tell my co-workers, some of which I manage, saying I needed to contact them immediately in regards to my delinquent on my account though I have NEVER been late. Not only is this embarassing but potentially damaging as I'm trying to get a promotion right now and Credit stability is required to move up. I would do anything to get rid of this company.

payment administration not in order

Nationstar took over our mortgage from Flagstar Bank. Apparently, they did not receive full records from Flagstar and concluded that I did not have homeowners insurance. They automatically instated a ridiculously expensive insurance and established an escrow account on my behalf to pay for it. Even though I submitted proof of insurance (with the excellent help of my insurance company, Liberty Mutual), they kept the escrow account and the insurance active. After many calls, when they finally canceled that insurance (for which I even had to sign a release form), they kept my escrow account balance and started charging late fees. After numerous more calls, they finally canceled the escrow account too, and sent me a check for the balance...! I immediately paid that amount back to them (as they did not owe me anything, and I want to be current at all times).

Yet, my account still shows a balance (the old escrow account balance plus late fees), even though I have always made all my payments in full, on time. And for months now they keep calling me daily about my balance. And I call them back every other day or so! And every day they assure me that they will correct the problem. But it never happens!

Either they have a serious issue with their administration, or this is a scam. In any case, I consider this harassment.

I have an escrow account that was carried over when NationStar bought my Flagstar loan. However, NationStar didn't pay my homeowner's insurance. It was due on the 15th and is now 11 days overdue. My insurance company called them to ask why the payment was late, and NationStar said that they weren't responsible for paying it. My insurance company called and told me to pay up or they would cancel my homeowner's insurance. I called NationStar and they told me that my condo association pays my homeowner's insurance. What?! I told them this was nonsense as I'm in a stand-alone house. They are responsible. I had to wait on hold a lot and talk to several people, but I remained insistent that they were responsible for my homeowner's insurance. At first, they tried to say that there wasn't an escrow account, but I pointed out that they'd recently increased my mortgage payments to cover the escrow "shortage." They are saying they will "do research" tomorrow and then "overnight" a check, which "may" arrive by next Tuesday. They are also promising to write me a letter stating that they made a mistake and that they will pay my mortgage in a timely manner in the future. We shall see.