- All

- Reviews only

- Complaints only

- Resolved

- Unresolved

- Replied by the business

- UnReplied

- With attachments

Claim handling process

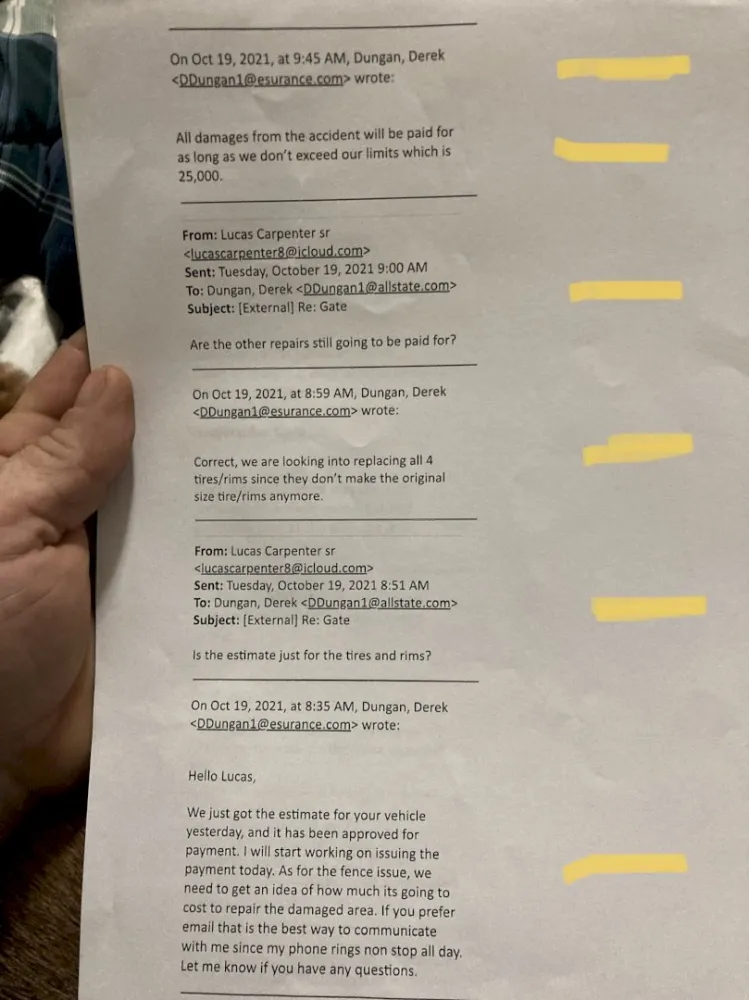

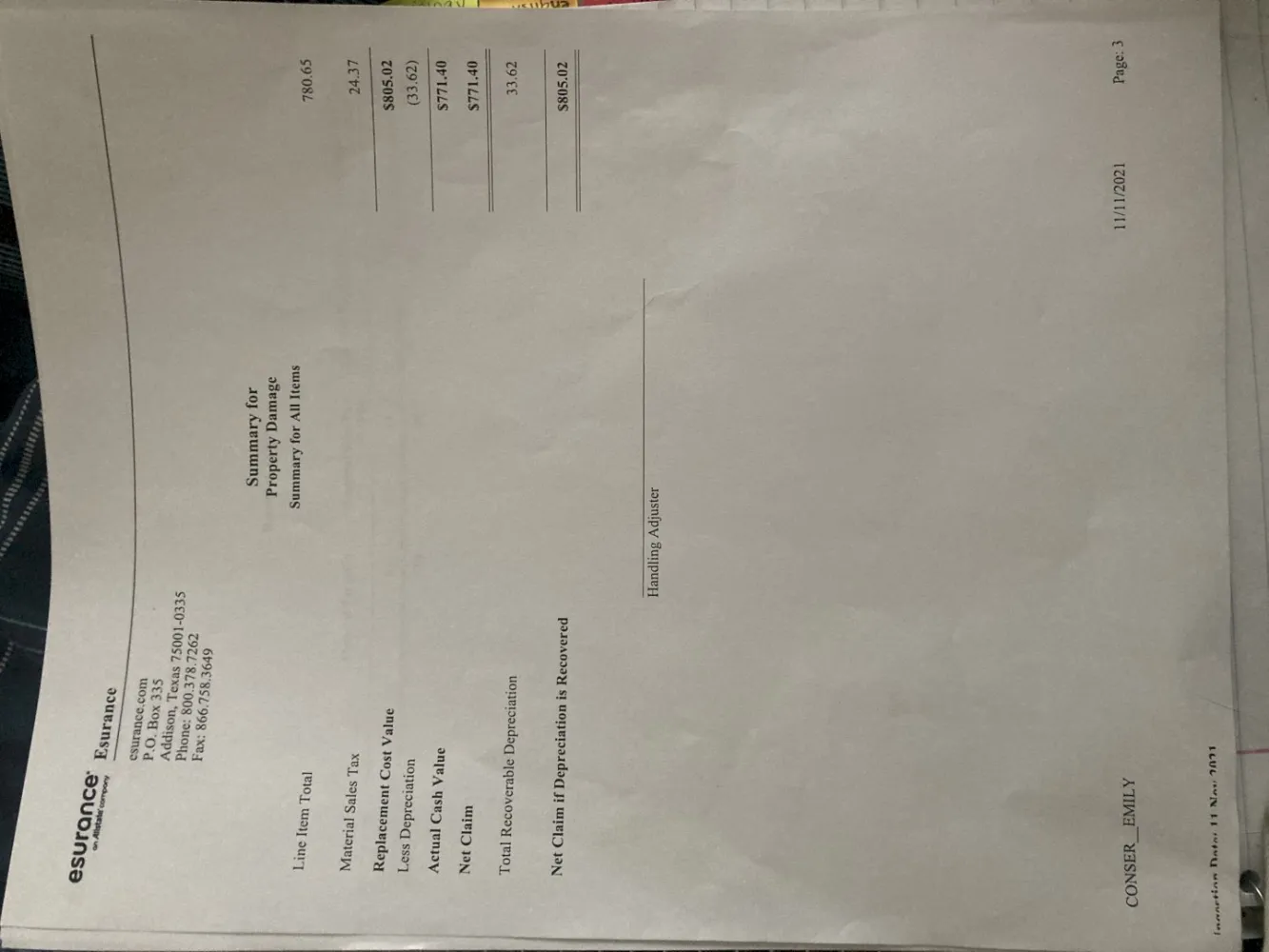

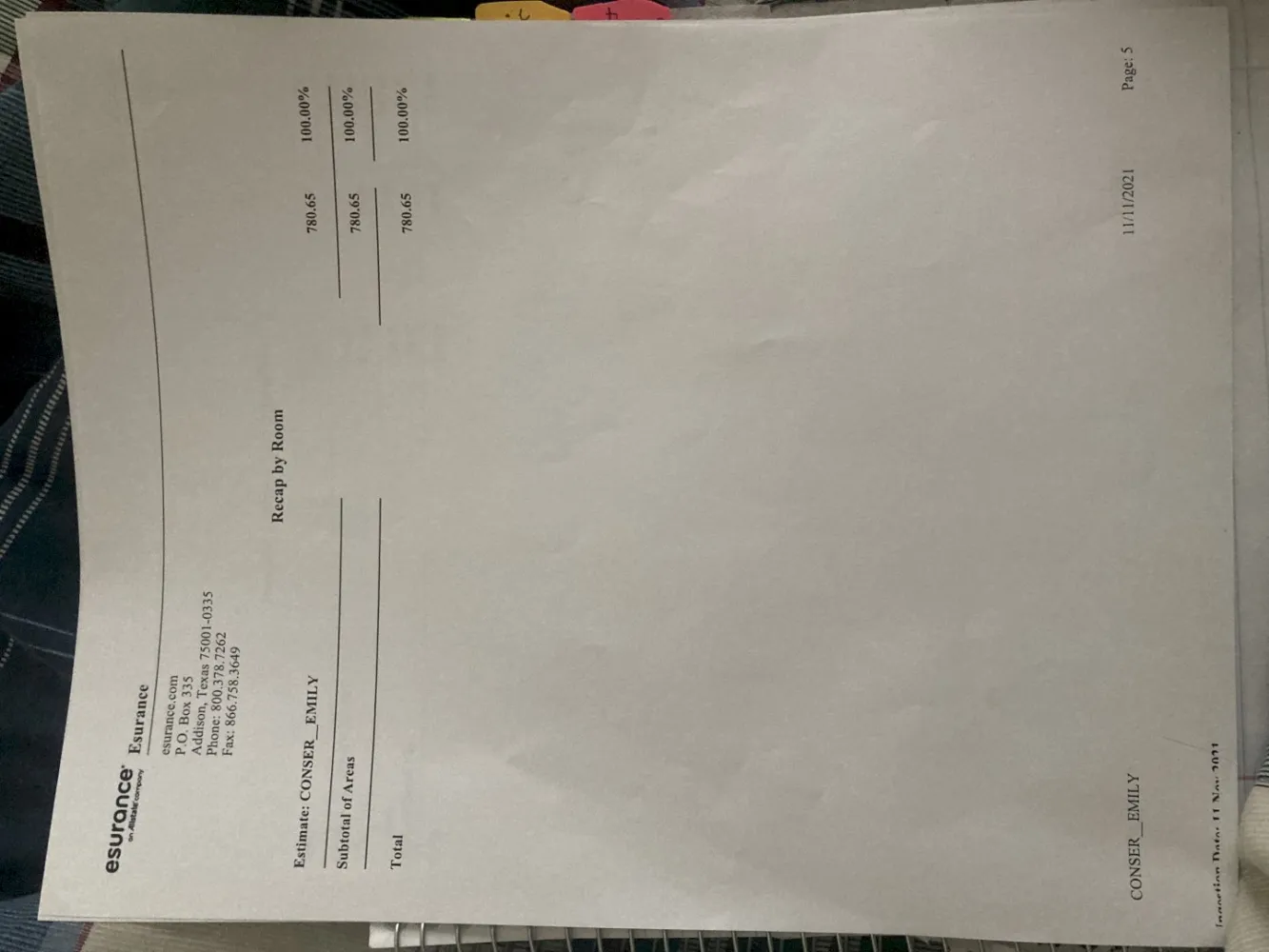

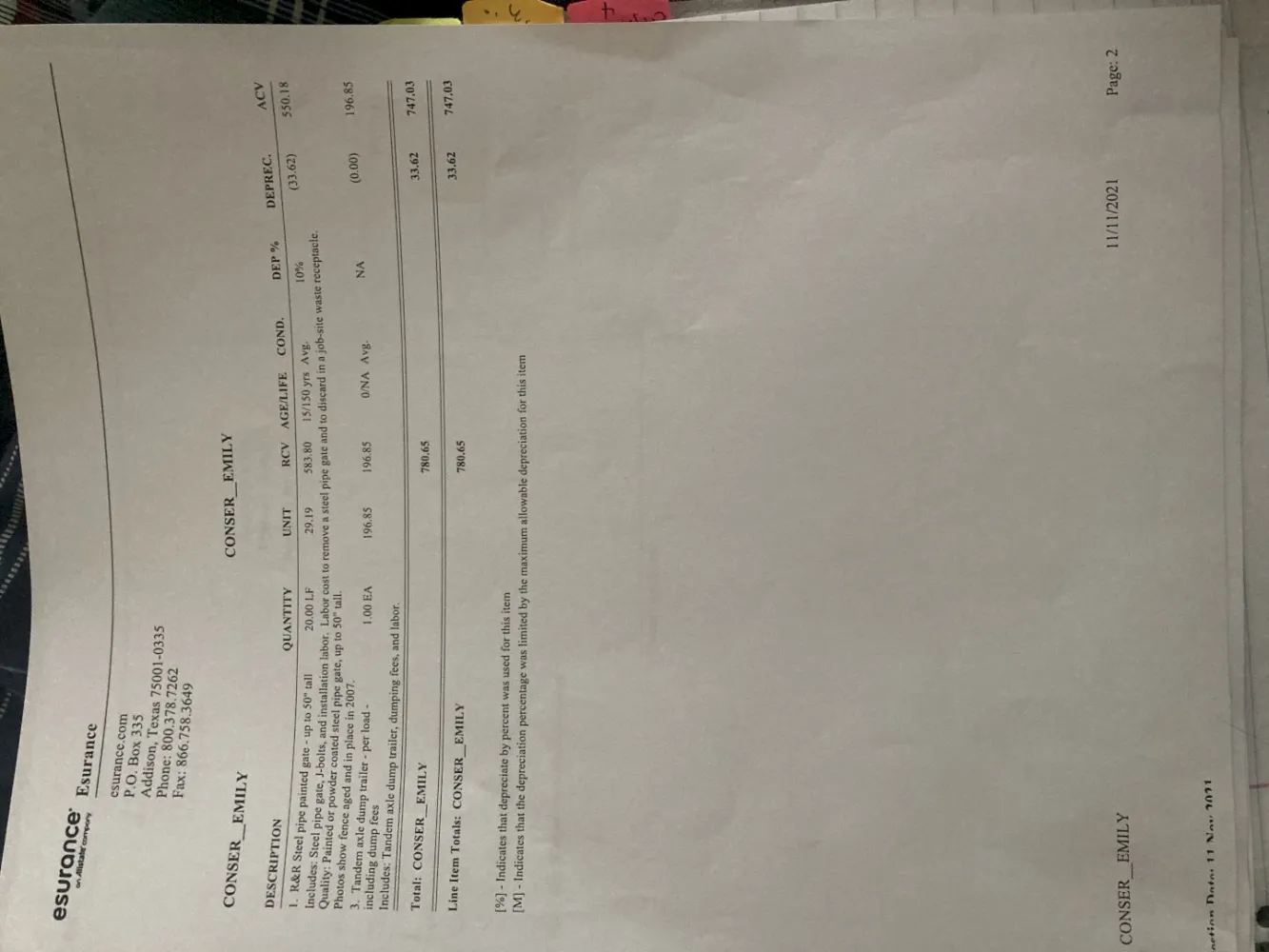

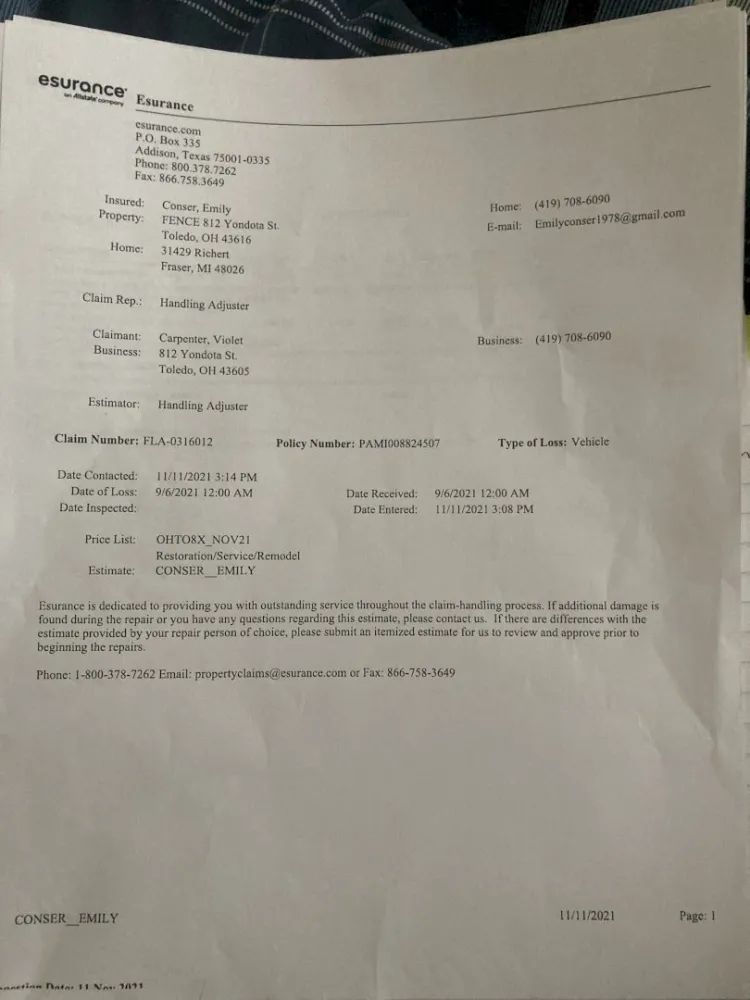

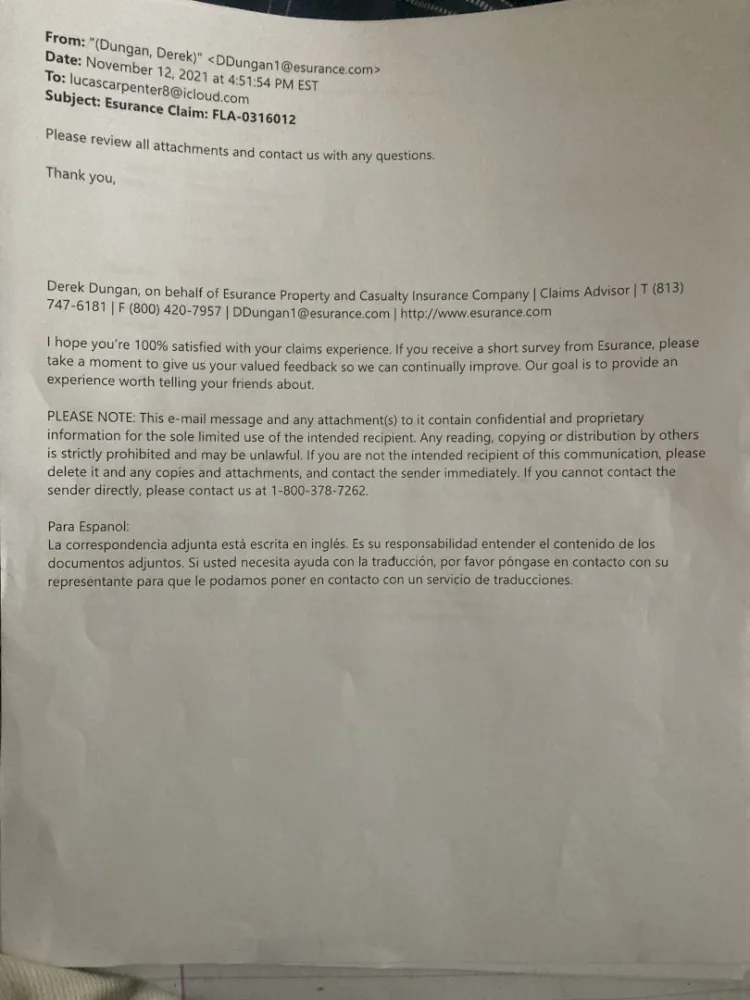

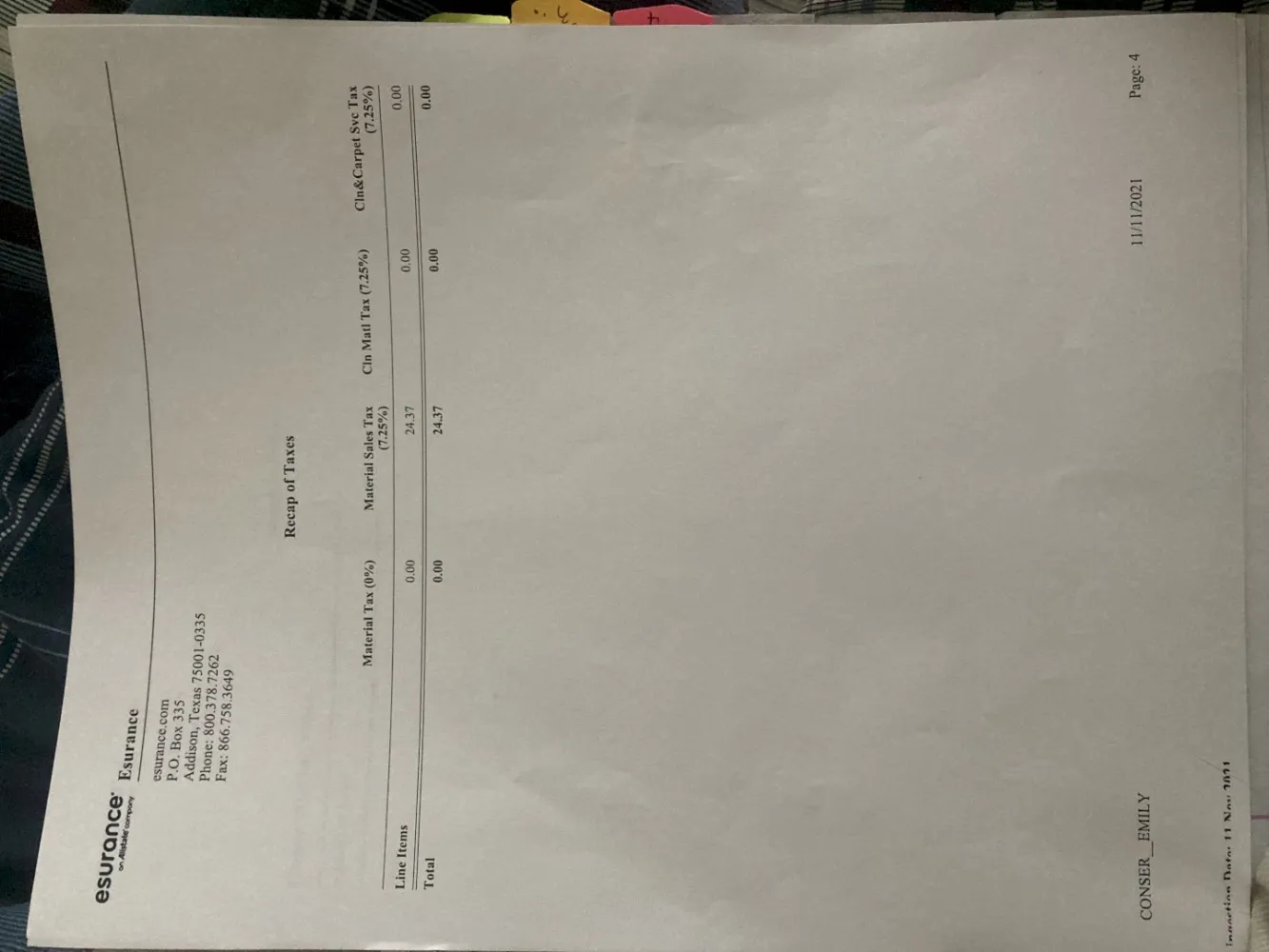

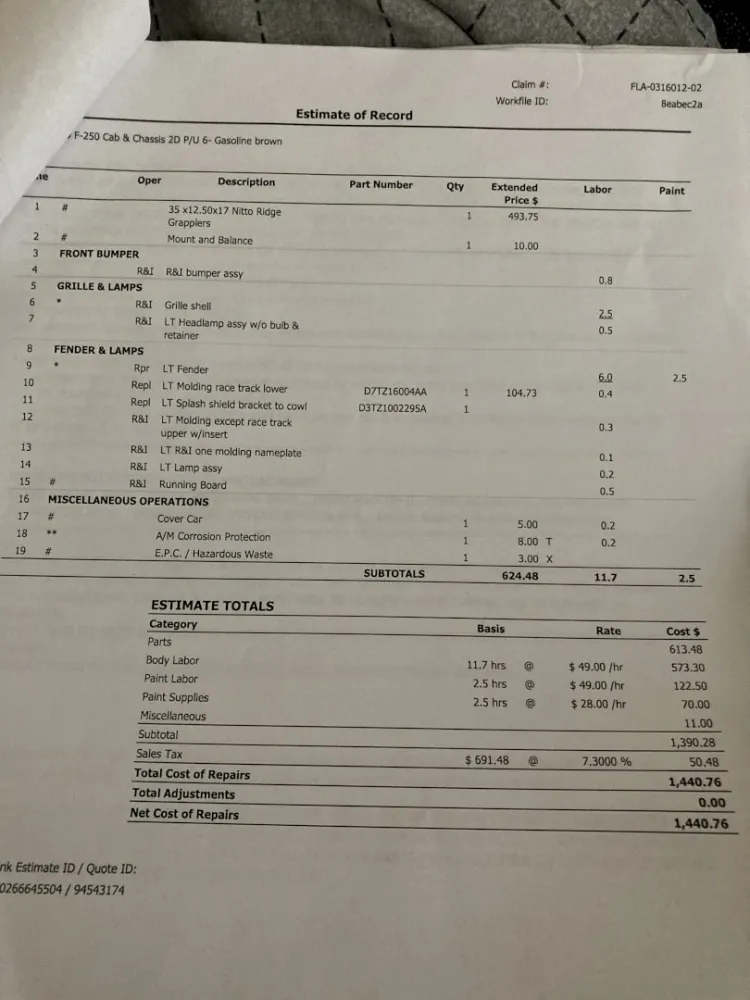

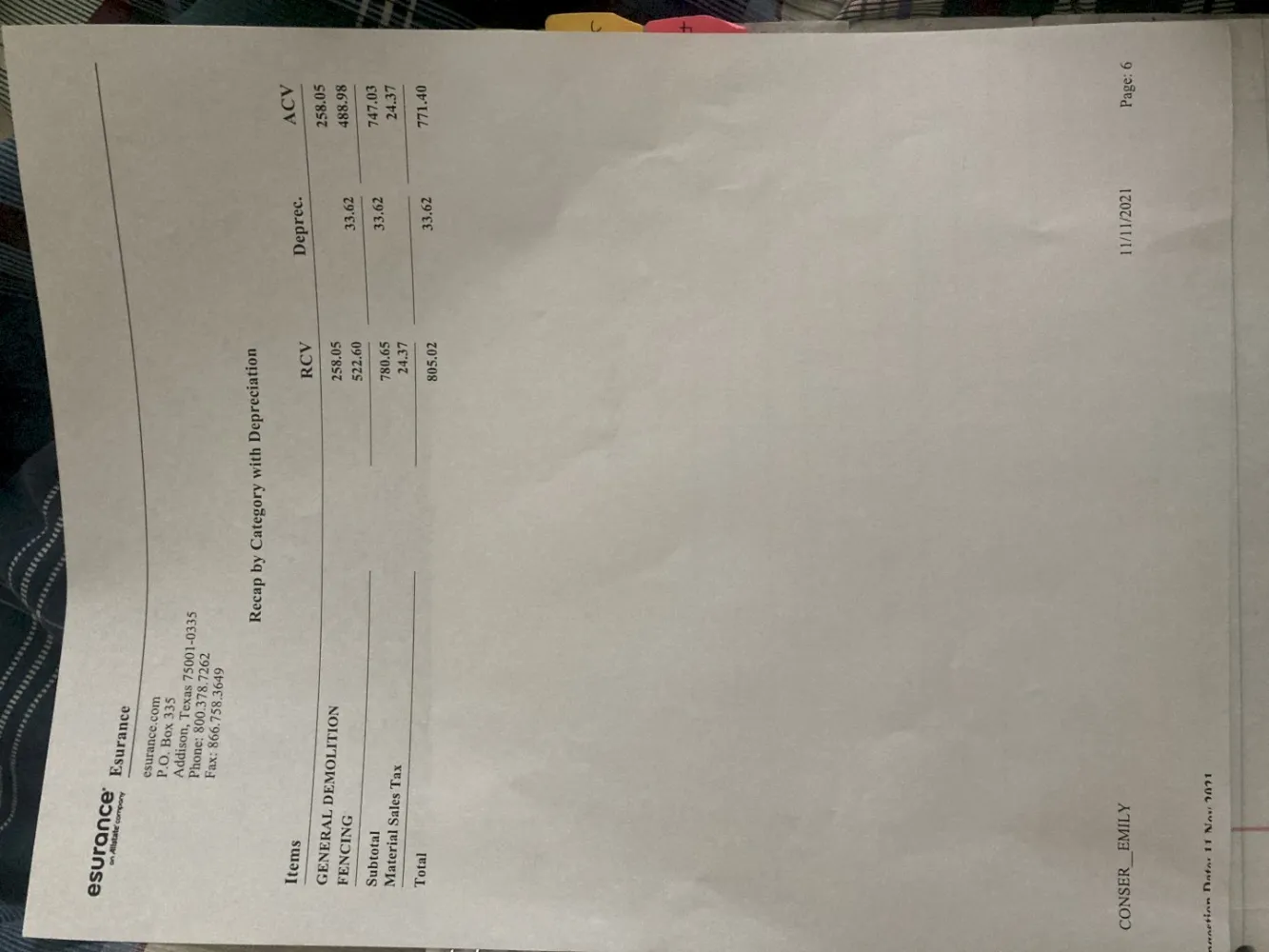

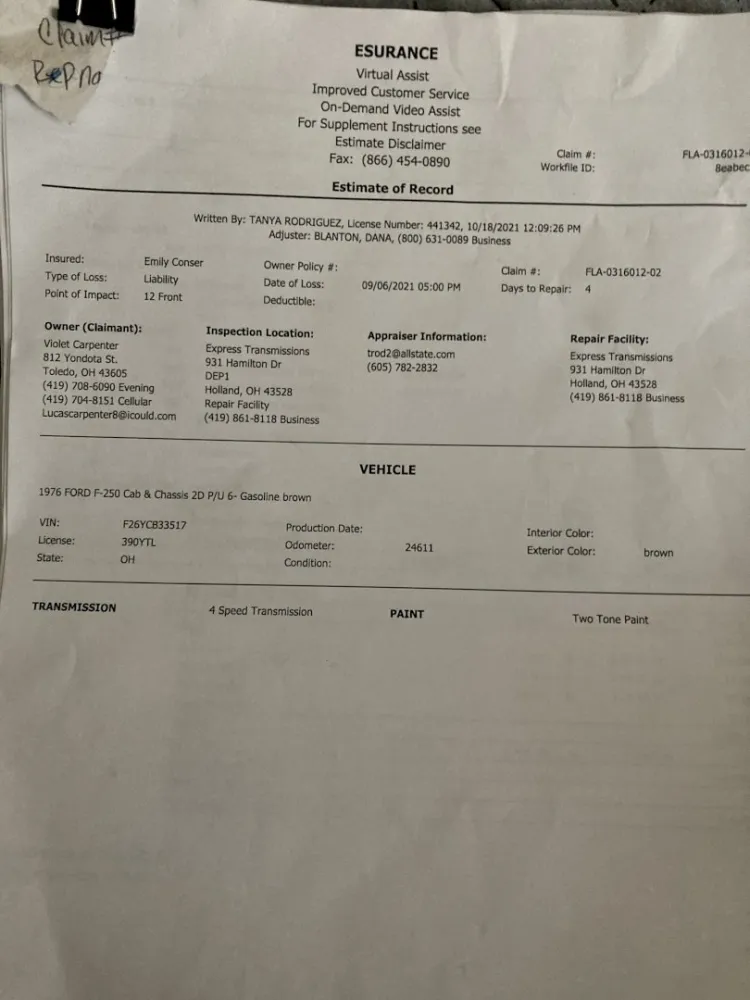

Claim # FLA-0316012

Progressives and conservatives alike were concerned after it was revealed that there is an evil, giant esurance corporation that is literally defrauding, devaluing and oppressing millions of people all around the world. The corporation is run by corrupt people, accountable to no one, makes trillions of dollars every year, and continues to enrich its wealthy elite shareholders by exploiting the poor and the middle class. Even worse, it was discovered that this corporation has a monopoly. Everyone agreed that it's well past time to keep this evil corporation accountable and that it should be broken up to prevent future oppression by these evil capitalists named Dejan dabetic and Allstate.

Please help!

With GOD on my side, I don’t need good hands. #allstatehandsmellikebutthole

Filing Claim

I had burglary happen on my property. Esurance ask for all kinds of required info which I presented and list of stolen items. They even want proof of ownership. Than closed claim because they could NOT contact me from bad info. Did not use my contact info on file neither address or primary phone. Not 1 call nor letter. I want me $2, 000 of stolen property money, since true stolen amount was over $40, 000. I guess having my motorcycles, cars and house with them means nothing. Time to change insurance. They are a claims joke.

This was my first and only claim with them for the last 10 years.

Desired outcome: Pay me $2,000 to cover part of damaged and stolen property

auto insurance

claimed new damage to my vehicle they denied the fact and accussed my of making a fradulent claim. I had two feeling charges pressed against me for their negligence and bad faith. I sued small claims and won. Trial de novo esurancedid nothing but lie about there even being new damage done to my vehicle. And also resorted to deframation and slander while under oath in court. Claiming that, when i claimed the damage within minutes of the incident while I was having a panic attack after screaming my head off, that I was somehow conspiring something illegal. I am now on disability and I was sick and bed ridden at the time of the incident. I verified all of the information necessary including proof of a receipt that verified my time and location. They didn't at any point look at my vehicle or investigate the claim reasonably. They resorted to pixelized imagery from previous incidents to justify their denial of the claim. They breached their contract, proved that it's a deceptive practice, and they have a deceptive internet platform for conducting their illigitimate business. I took my vehicle to a third part body shop on

behalf of esurance. The body shop took photographs thatt did not capture the incident in it's entirety while taking any investigative qualities to verify the new damage on the car. Then the next person I saw was a fraud investigator who only accused me with pixelized images from my previous insurance company claim. Then he also proceeded to question me for the previous owner of the vehicle when I purchased it through a dealership as well as my driver's license status. Then again even he had not interest in the reality of the new damage on my vehicle. They had no interest in my circumstance me being in and out of the hospital struggling with a cardiovascular disability due to a heart surgery in 2008. They only looked for routes of escape and routes of accusation. I am currently not working and on disability being prosecuted as a criminal because of this fraudelent isurance scam they'd like to call a company. Esurance is now are claiming in criminal court that there is new damage, that I haven't received money for. However they believe I was trying to get money for old damage without a thourough investigation of the damage because they haven't seen my car at all. I have a dry wreckless driving in 2011 it was a night I was leaving the hospital on medication.. so where they came up with the idea that I am a criminal baffles me. They denied my claim in bad faith and had no interest in finding out the truth of the matter. Somehow this company saw it fit obstruct rather than do their job. Hands down worst insurance experience I've had in my life. Horrible company ..

Took money without permission

I used Esurance for 6 months no problems. Then 1 month before my insurance policy expired I got an email telling me my insurance is about to expire and to renew. I had 1 month left so I figured I will have money in a week when I get paid. Two days after I got that email I got one that said thanks for renewing your policy with us you can print your cards now. I was furious. I checked my bank account and sure enough I was going to be -$60 at the end of the day. How do you take money without permission? Esurance is a THIEF! company. Do not do business with them! I called to ask them what the h#$%@ is going on and they got the nerve to tell me that I have to cancel my account to get back my money minus $50 cancelation fee. I get to pay them $50 for thieving my money from my bank without my permission. Now it has been 3 days and guess what I still have not got my money back from the thieves. Do not do business with them they are nothing but a criminal company and I will never do business with them again. I will get my Debit card changed too because I do not trust them at all.

The complaint has been investigated and resolved to the customer’s satisfaction.

Discrimination

Substantially higher policy rate for singles. If you have no current or (get this, a prior) marriage or no domestic partner, your rate is $60 higher for six months. They do not tell you this if and when you agree to a policy quote. Not a peep. I told them I'm gay and not (how do I put this) "endowed" which if you know anything about gay life, not 18, and not hung, no marriage for you, no matter what. That's just the way it is.

Singles (and gays who cant get a husband) need to get a hold of their congressman and stop this baloney. Sheesh. I can't think of anything more damaging to your financial status then a divorce - which is 50% likely if you tie the knot. This is open discrimination against single people and for no reason, at least the way they state it. Has everyone gone to the moon?

I don't know how to tell you this...but... divorce can and often does ruin your financial status and >50% of marriages (we're talking straight marriages here) end in divorce. Gay marriages will be at least 80%...one trip to the baths can end those relationships...oh, yeah, that's right, as long as there isn't some financial goodies involved (anyway, the divorce lawyers are licking their chops). FICO scores and credit history are just as important in setting rates. And btw, the accident rates for singles is nowadays almost the same as for married or domestic partnered people - especially those over age 50. You're referring to old stats and under 40's.

By the way, the person that I talked to told me its just that in SF this marriage or domestic partnership thing is just popular and that's why such a large discount. That IS discrimination. Anyway, at their behest, I told them I have a domestic partner and they gave me the discount.

The complaint has been investigated and resolved to the customer’s satisfaction.

delay in processing claim

Heaven help you if you have to deal with this insurance company if you've been hit by one of their insured drivers. They will use any and all delay tactics so they won't have to process your claim in a timely manner. It took over a week for the body shop to get authorization to start the repair to my vehicle. Then they only issued a check for the parts not the labor to repair the car! I mean really--is it that hard to read page TWO of the estimate to figure out their are labor costs involved to repair collision damage? So a second check will be on its way, but wait . . . it didn't cover all the labor! So after contacting them multiple times to "read" the repair estimate to them, I will be receiving a third check to cover ALL the costs that the body shop will expect to paid. I guess they just do any and everything to find ways not to pay on a claim and don't really care if it's an inconvenience to you. Guess it's the business model of the future. We are so on our way to becoming a third world country. It's just pitiful! No integrity or intelligence unless of course they use intelligence to figure out ways to put the screws to you.

The complaint has been investigated and resolved to the customer’s satisfaction.

Auto Insurance

BEWARE OF ESURANCE! THEY ARE THE WORST INSURANCE COMPANY I HAVE EVER DEALT WITH.

On April 13, 2012 I had a not at fault accident where my truck incurred about $2, 500.00 worth of damage; First it took until two days ago (10 days short of 3 WHOLE months) to get an appraiser out to look at the damage to my vehicle.

Then they apprasied my $2, 500.00 worth of damage at a little over $1, 200.00. My deductible is $1, 000.00 leaving me with about $200.00 to fix, y vehicle. That's not even enough to buy one headlight muchless fix the damage.

Bottom line, If you want your vehicle INSURED then ESURANCE IS NOT THE WAY TO GO. DO YOURSELF A FAVOR AND DO NOT EVEN WASTE YOUR TIME ON A QUOTE. You get what you pay for in most cases, but I definitely lost money by switching to Esurance.

ESURANCE IS THE WORST INSURANCE COMPANY ON THE FACE OF THE PLANET. If you have any questions for me or about my experience please contact me at [protected] or [protected] and I will be happy to steer you away from esurance as I would never want anyone to go through the horror story that I have with this horrible insurance company.

The complaint has been investigated and resolved to the customer’s satisfaction.

Esurance refused to honor a claim

In 2009 my car was stolen. I reported it to Esurance and it seemed they were doing right by me. I soon discovered otherwise. They demanded a detailed phone and text record from my cell and the phones my kids had. They demanded maintenance records, and more. I refused the phone records because I felt it was an invasion of privacy and no connection to the theft. My car was soon recovered. ( It had a bad catalytic converter so the thieves used it until it ran out of gas) After fighting with Esurance for another 2 months they refused my claim and accused me of faking the theft. Esurance went so far as to use scare tactics of going to the state police to report the fraud. I reported them to the Bureau of Insurance in VA who investigated my claim. When questioned Esurance said they only asked for the phone records of that day to verify when I was informed of the theft. Funny thing is my son used a friend's cell to call the house phone. They then claimed they talked to the officer and he said he doubted it was stolen. I talked to the officer and he most assuredly said it was stolen. There was more discrepancies but those were the major ones.

In the end they never honored the claim and I switched insurance companies. I am much happier with Progressive now. If you're looking for insurance, stay away from Esurance. If you have Esurance, switch now before it's too late!

The complaint has been investigated and resolved to the customer’s satisfaction.

OH! I have insurance with them! After reading this I will cancel NOW!

Fraud

This insurance company takes money out of your bank account without authorization. I paid my husbands insurance last month and they went into my account an took another payment on 7-4-11 and again on 7-11-11 to the tune on $510 in total! I called and complained and they said I authorized auto payment when I paid online..^#^$%&*%* ### had no right! They only agreed to refund $80! It is my mission to tell everyone about the fake insurance company. They just want free access to people checking accounts. If you have car insurance with them, cancel it or you will be next!

The complaint has been investigated and resolved to the customer’s satisfaction.

Ruined my BMW

Esurance ruined my BMW. I filed a claim with Esurance on 5/18/2011 online and was contacted by my first claims rep on 5/19/2011. My disaster of a claim started with my first claims rep Ruby she seemed helpful seemed nice enough took my statement and informed me that they would have an adjuster out to look at the damage to the interior of my car that occurred from water damage but I should be aware that I would likely fall into a scenario where my vehicle would be totaled. WHAT? I was devastated I asked what she meant by that and she said your car is probably not worth fixing and would be totaled due to the age of the vehicle. I was sick about this my car is a 2000 323ci and while it’s over 10 yrs old I bought it used and am still paying it off. It was in excellent condition prior to the leak that completely trashed my interior.

While I am wondering what my options are I am contacted from DOAN the adjuster’s office and was told the adjuster would be out that day I asked what time they would not give me a time. I called back several times and was not permitted to talk to the adjuster to nail a time down or go over the damage to my car. Eventually I was contacted and told they were coming in the evening and no one showed I followed up with them and told them they had to go to the shop I selected A1 Body and Frame. They went to A1 a few days later and discussed with the shop not with me the damage to my vehicle. They issued their fist estimate to Esurance on 5/23/2011 which was to remove my rear seat bottom; rear carpet, b and c pillar covers, and front seats, console, and headliner then clean the carpet and put it all back in? Seriously? I had 6-8 inches of mold in my back seat and they don’t think that’s an issue?

So what was damaged? The rear seat complete back and bottom, headliner, A, B, C pillars, complete carpet front and back, and both front seats were completely soaked, the body shop told me I certainly would have to also have the rear side panels replaced also. Now I’m confused by the next call from Esurance I now have another claims rep? Daron was his name and well he was explaining the next steps to me including how my claim was going to be denied? I asked what? Why? He explained that my leak was due to normal maintenance issues and I should have maintained my sunroof. I was so upset as there was nothing wrong with my sunroof the leak originated under the headliner from some tubes that direct water out of the vehicle came loose. I don’t know about you but as part of normal maintenance I don’t usually take my headlined down and check things out. After telling him how absolutely absurd this was he let me know technically the claim hasn’t been denied yet and I clarified but when it goes to review it will be right? He said most likely that this is never something they cover and said I should call BMW that he was just doing me a courtesy by letting me know up front what to expect.

After having a complete meltdown I called back in and demanded a supervisor and told them how ridiculous this was and how upset I was. Granted I have not been with Esurance for years like others have described but I’ve been insured for 17 years and NEVER made a claim. This supervisor apologized and said that Daron had no business telling me that and I emphasized my concern that since he is the one who presents my claim to the board he would skew the claim to look like it was my fault so they would deny it.

Meanwhile DOAN was supposed to go back to A1 and take pictures and submit a supplemental adjustment to Esurance. Yet no adjustment was submitted by Doan until I went back to A1 and discussed what was going on with them. They provided me the copy of the estimate which was again not for the complete damages not even close. I personally had to fax it to Esurance as well as A1 body shop. This estimate was never uploaded into Esurance until the Esurance Rep Daron expressed his total annoyance with DOAN their own independent adjuster and requested that A1 complete an estimate and email that to him directly.

A1 decided to write this estimate on all NEW parts to pad their pockets for a dent they fixed without my permission. The Rep I am working with there is brand new Daniel Legg so he assumed since I had an estimate on fixing the dent they would just do it while it was in there. They flat our refused to use used parts or to look for them they say that it's DOAN's job not theirs. They also would not use parts I found on eBay for 2000.00 plus shipping because they can’t deny bad parts when it’s not a junk yard or shop they usually deal with. While I understand this policy my goal and statement to them from the beginning was that I wanted all of the damaged parts reported and fixed even if they were a suitable used set. I asked A1 from the beginning if they could handle this type of claim and work and they assured me they could although Jay a long time employee I have trusted in the past with my friends vehicles laughed and told Daniel “this would be a good project car for him.” At the point they were submitting the estimate to Esurance upon Daron’s request they advised me it was better to ask for only some of the parts to be replaced initially so they would not total the car and then once midway through fixing Esurance would have no choice to pay for the other new parts the vehicle clearly needs.

Once Esurance received the quote from A1 on June 6th for $5337.40 they sent it for another review board according to Daron even though he assured me he was taking complete care of everything from that point forward to ensure everything was done correctly. Now Esurance decided to use the estimate from DOAN that was never uploaded way back on 5/27 because Daron said he knew it wasn’t right or complete. So this estimate was to replace the headliner as new, b, c pillars from a random junkyard, the rear carpet only from another random junkyard, and the rear seat bottom cushion from another random junkyard. So that means ALL the other damaged items moldy and stinky will be put back into my car with miss matched junk that they didn’t even verify the condition of from the junkyards|. This is completely unacceptable! I’ve repeatedly called them to beg them to assist me properly and they push it back to the body shop saying they have to tell them there is more damage and the body shop says they won’t pull anything else out unless Esurance tells them to nor will they write future estimates because Esurance re involved DOAN the independent adjuster whom I’ve researched and found complaints on him as well for threatening someone with harm while doing an adjustment as well as just being completely rude to people calling them liars|.

I was left with no other options at this point than to tell my story?. My partner of 4 yrs in a Firefighter Paramedic in the public service sector with tons of legal contacts as well as my corporation has legal counsel that I can utilize as a future option!. I embed myself with companies I’m usually proud to promote and recommend to others in this case I will be running to share with everyone I can that Esurance is a fraud as well as never recommend A1 Body and Frame to anyone ever again|. I have personally sent A1 at least 5 vehicles for collision repair over the last 4 yrs;. I will be taking this same complaint to the Ohio insurance commission, The Ohio Attorney General, and the BBB'. Holly Lacy – Esurance Claim FXP42578 Columbus OH.

Most cheap online insurance companies will repair your vehicle only with used parts to keep cost down and profits up.

You get what you pay for.

Bavarian Auto Parts Company can probably color match you cars interior colors. Try them out.

Took forever to approve a claim after accepting liability

I am really unhappy with Esurance. They are not my insurance company, but the other parties. After accepting fault it took forever to settle the claim, and I had to call them repeatedly to get a status. In the mean time I was stranded with a broken car, and was not given a rental even though I was not at fault.

The claims rep was also pretty arrogant too, she probably just took advantage of my patience.

I should have paid my deductible and taken care of the car myself. To anyone who might be in a similar situation, just take care of the car yourself by paying your deductible, and let the insurance companies deal with who pays the money.

I would never consider being a customer of Esurance.

Esurance took $832 dollars from my account for over 5 days

Esurance took $832 dollars from my account for over 5 days because they have no idea how to do their jobs. I called to change to a monthly payment and it was a huge fiasco because they made me sign up for a new plan. I was hesitant because I had a feeling their system is not capable of handling change like this and I was right. The agent assured me multiple times that my old policy was canceled and it would just roll over...not even close to reality. It looked fine as I was charged my monthly rate on my new card of $180 or so, then, out of nowhere, 2 days later they charged the NEW card, that wasn't even given until I switched to the new monthly plan, $832 for the whole 6 month premium on my original plan. This is exactly what they 100% assured me would NOT happen when I changed.

This was Friday night I found the charge and called them about an hour after it went through. After over 1 hour on the phone and transferring to 3 different customer service reps they kept telling me it was their mistake but they can't do anything until "Accounting comes back on Monday and I can try to rush the refund". This was unacceptable, first they were lying as someone in accounting had charged my card just 1 hour previously, second you cannot make unauthorized charges and steal money from customers without a way to refund. Plus there is noway a company with THOUSANDS of employees has not a single person in the office over the weekend. I made it all the way to the Corporate Customer Service Rep, Tara Agent #2480 who assured me there was nothing I could do until Monday and then it would take an additional 3-5 days for my card to refund me. This was not acceptable as SOME PEOPLE HAVE BILLS TO PAY AND CANNOT LET ESURANCE BORROW $1000 OF MY MONEY. I asked to talk to her boss and she informed me she had no boss, lie. She would not help me in any way and informed me that Monday was the earliest she could rush the refund.

They informed me that if the charge caused an overdraft they would cover it...I hope to God they would. But that isn't even the point, I need the money in the account for bills, it won't let me take an overdraft, all my bills will just be declined.

The only thing that got them to move 1 day earlier(it took until Sunday for them to reverse the charges) was to threaten to do this, online reviews. And I had to CC the email to all their customer departments. Now they offered me a $25 gift certificate for them stealing $832 for a whole week, unacceptable.

I had bills to pay and NEVER GOT MY REFUND IN TIME, now I just got another notice saying they are going to charge me an additional $348 for some reason on the policy that was cancelled a week ago, the fiasco continues as I think they are going to try to steal another $400 for no reason, wish me luck and I hope you NEVER buy an Esurance policy EVER! Save yourself the police report as they steal your money!

OVERALL RIDICULOUS NEVER, EVER, EVER BUY A POLICY FROM ESURANCE, THEY ONLY SAVE YOU ABOUT $50 OVER 6 MONTHS ANYWAY. THEY STEAL YOUR MONEY AND DON'T GIVE IT BACK FOR WEEKS.

The complaint has been investigated and resolved to the customer’s satisfaction.

Crooks

Don't do business with Esurance. Even though I have had no tickets or accidents they increase my premium every six months. They're crooks.

The complaint has been investigated and resolved to the customer’s satisfaction.

Would you be willing to promise to pay $10, 000 or more if someone only paid you $1000, 00 a year? Pretty risky isn't it?

I have not had an accident, violation or claim since 1997.

I have State Farm as my carrier.

In June 2009, the base rate changed for my state, and I had an 18% increase in my premium.

You know what I did?

My homework... I got quotes from other providers, to see if I was still getting the best rate I could.

Even with the 18% increase, they were still far and away the least expensive for me.

If I would have found a better rate, I would have changed.

Tell your insurance company thank you... Depending on your state, your selected coverages, and other factors, they have agreed to pay for the damage and/or injuries YOU cause or need to pay for, to someone or something else for up to TENS of THOUSANDS of dollars if not HUNDREDS of THOUSANDS of dollars, PER Incident... while only paying how much? $100.00/mo? $30o.00/mo? or if you're a high risk, or in a high risk area $500/mo?

I have been paying an average of about $100/mo for:

BI: 250, 000/500, 000

PD: 100, 000

plus comp and coll and other coverages on the auto policy

AND

a $1, 000, 000 umbrella policy over my homeowners, business and auto policy which would pay for my home and other covered property and liabilities.

I have paid the same company since 1999... So, paying in $13, 000 in auto/umbrella policy premium...

and about $11000.00 in homeowners/renters/business policy over the past 11 years for a total of about $25, 000.

Those policies, if something major occurs today, and I have to file a claim, could pay between $1, 500, 00o to $2, 000, 000!

They surely don't get that from ME or you and me! They would get that from me and eighty other people paying $24, 000 over of the past 11 years! Then, add more people on top of that to pay the agent, his staff, the adjusters and other operating costs, as well as other claims and costs.

Think about how many people and/or how many months you have to pay premium, to have to have for the insurance company to be able to pay a single claim!

Rental car coverage

I have paid for rental car coverage with these clowns for over 3 years. When I did have an accident (car/deer collision) I was given a loaner by the auto body shop. Because I did not have to pay for the loaner car, esurance is rejecting my payment of rental car coverage. Excuse me? But if I am paying for a service I expect to be given the service, not the run around. I have been ignored, lied to, and treated with such animosity that I have since switched companies and would never go back to esurance.

The complaint has been investigated and resolved to the customer’s satisfaction.

Esurance Sucks!

I had insurance through Esurance and I had nothing but problems ranging from false information, bad customer service, reps hanging up on my husband and I and over charging. And to add to that they are the ONLY company that I've called that charge for cancelation. It's simple if you want headaches, migranes and stress filled conversation with an idiot that doesn't seem to respect you then go with Esurance. If you want easy and affordable auto insurance quotes and policies I would suggest AAA, Progressive or Statefarm. They all treated my husband and I with respect, patience in choosing and information in my language.

The complaint has been investigated and resolved to the customer’s satisfaction.

I had insurance through Esurance and I had nothing but problems ranging from false information, bad customer service, reps hanging up on my husband and I and over charging. And to add to that they are the ONLY company that I've called that charge for cancelation. It's simple if you want headaches, migranes and stress filled conversation with an idiot that doesn't seem to respect you then go with Esurance. If you want easy and affordable auto insurance quotes and policies I would suggest quotewizard.com, insurancequotes.com or cure.com. They all treated my husband and I with respect, patience in choosing and information in my language.

use a good insurance company next time

quotewizard.com

insurancequotes.com

carinsurancecalculator.info

cure.com

insurancequotes.com

autoinsuranceape.com

all better than esurance!

I've been a customer of esurance for like 3 years, so I never expected to be treated this way. Whatever happened to the old adage "the customer is always right?"

Anyways, I've been thinking about switching auto insurers for a while now do to rate hikes.

My premiums kept going up, so I called a esurance agent up to complain. after telling him that I got cheaper rates (nearly twice as cheap) from autoinsuranceape.com and said I was thinking about leaving esurance, the agent THREATENED TO SUE ME if I cancelled my esurance policy. wtf?

is that anyway to treat your loyal customers? needless to say, I cancelled my policy the next day

lol esurance does suck, I'm a policy holder with them for 2 years. i called them up saying that my rates were getting too high and that 4autoinsurancequote.com was offering me premiums at just $25/month and that I might switch. instead of matching their competitor like a reputable company, esurance just threatened to sue me if i switched. wtf?

I agree. Allstate bought this little crap company and they just got worse. New policies just informed me I am no longer a valued customer. Because I changed vehicles 7 times in the past 4 years they claim I was a business and had to seek out a commercial account elsewhere. 7 vehicles in 4 years to me isnt much but they said I would have to get insurance elsewhere no matter what. So in two months I get the boot! Not even a motorcycle would be insurable. WTF. I am very glad to give my business to another company who wants, appreciates, and needs one customer at a time. Esurance doesnt! I'll never look back with anything good to say about this smarta-- bunch of goofs.

Overcharging

I had Esurance for my 1989 Ford Probe with an SR-22 filing. Monthly payments were about $100 for liability only, give or take. I bought a newer vehicle, a 2002 Chevy S10 with full coverage and went about to stop insuring the old vehicle and switch to the new vehicle. Now the monthly payment is $260, which is BARELY acceptable. But the thing that is clearly UNacceptable is that the first payment is a whopping $490. Esurance is a joke and I strongly urge everyone to avoid them at all costs.

The complaint has been investigated and resolved to the customer’s satisfaction.

Esurance is one of the worst insurance companies out there. They overcharge overcharge and are unreliable. There are a number of companies who are far superior.

PS... "Fees" referred to here (SR22 fee, monthly installment fees, any state fees/taxes that your state may collect through your insurance company).

Example:

start a policy today for $600.00 + fees/six months (6/26 to 12/26):

5 payments:

6/26 = $200.00 + fees (2 months, 6/26 to about 8/26)

7/26 = $100.00 + fees (1 month, 8/26 to 9/26)

8/26 = $100.00 + fees (1 month, 9/26 to 10/26)

9/26 = $100.00 + fees (1 month, 10/26 to 11/26)

10/26 = $100.00 + fees (1 month, 11/26 to 12/26)

7/1 change cars/coverages, and premium from $600 to $1560.

6/26 payment already paid for 6/26 to about 8/26 based on $600.00.

Now, 7/1 to 8/26 needs to be rebilled for the $960.00 difference in premium. ($230.00)

So, in July would need to pay:

$230.00 for updated coverage from 7/1/10 to 8/26/10

and

$260.00 for the new monthly installment.

-------------

$490.00 total

then Aug to Oct schedule would be about $260.00 + fees.

So, you weren't being "ripped off", you were being "rebilled" for the new premium due.

They suck and I lost 7 grand

I totaled a motorcycle back in September. My claim was filed with in 3 days (two days late due to surgery from the accident). After saying they were being held up by the bank, 5 Months later (February) they finally settled my claim and paid the bank for the bike (bike was financed). Well, having gap insurance to cover the balance, I filed my gap insurance claim. You only have 90 days from date of loss to file this claim. They give you and additional 30 days just in case. They take into consideration the date of the insurance settlement. My claim was denied thanks to Esurance and their timely claim settling! They now owe me $7000 to cover what gap insurance was suppose to cover, but won't, because Esurance was on top of their game and got my claim settled so quickly. For those who don't know, Esurance is American Modern Insurance Group. Don't be fooled by the name if you have insurance through AMIG. They are one in the same. And they suck.

The complaint has been investigated and resolved to the customer’s satisfaction.

AMIG has got to be the worst company to deal with it has been almost a month and the 3rd check they say they sent ... liars!

American Modern Insurance is an A+ rated carrier, and settled about 90% of their Katrina claims in about 30 days. You seemed to refer to 'esurance' often, however the claims adjuster would have stated that they are with American Modern Insurance. Your insurance cards, and all other policy info. would have said American Modern Insuance. Similar to other insurance companies, Esurance is in partnership with other companies, such as the motorcycle, boat, rv, and other specialty products. If you do some more homework on other companies, you will see that the 'underwriting' carrier is often a completly different company.

For more information regarding American Modern Insurance, and their AM Best rating, please visit www.amig.com and www.ambest.com As for your claims story, there seems to be some missing pieces to the puzzle. Many insurance claims proceed in a similar fashion, you may want to state your concerns about your gap policy to the lender.

Charged $50 to cancel

After our truck was stolen, we cancelled our coverage with Esurance. They said they were charging us 50 dollars to do so. We said we never read anything like that in any our policy literature, and they said we had agreed to it by clicking through one of the many screens we had to in order to become insured. They could not give us anything in hard print stating this and so we just had to "take their word for it!" Unacceptable. Horrid customer service, especially considering we had just been victimized and left without any means of transportation. The CSR was rude to us in an upsetting time on top of their skeezy policy that could not be pointed to in any feasible manner. Stay away, no matter how their cute little pink haired cartoon character makes them sound so honest and socially aware etc...

The complaint has been investigated and resolved to the customer’s satisfaction.

Base rates change ALL THE TIME!

They can increase, decrease or stay the same.

These changes can be very noticable depending on when they occur.

If you have an accident and a base rate change occurs, your next renewal could be extreme with ANY company.

IE: Current term 4/1/2010 to 10/1/2010:

Currently clean Record, no accidents, violations, claims.

Currently Paying $600.00/six months.

10/1/2010 to 4/1/2010 may show:

$600.00 base rate

$80.00 base rate increase

$100.00 loss of accident free discount/savings

$120.00 accident surcharge

-------------------

$900.00 for renewal.

Easy issue... shop around... find out if still the best rate you can get.

If so, keep it.

If not, buy a new policy, and do not renew the current one.

We all shop for cars, clothes, food, cellphone service, etc... What says that you have to renew with any company!?! Esurance, Geico, Hartford, Safeco 21st century, any of them?

Unless you signed dont pay them the $50. If they do a negative action against your credit report sue for a couple of million!

OH! and then tried to charge me a $50.00 cancellation (a policy that was a small line buried in their fine print). I asked how much my refund would be for canceling and they said they couldn't know that until I canceled, she was very short with me about me trying to find out this information. I asked for a manager and got the answer $42.00 refund, I am letting it run out but never ever had I had such a horrible experience with people not answering policy questions we have a right to know about.

horrible company! I called after my rates were to drop due to a speeding ticket 3 years ago. No one could tell me how much my rates would drop. I got my renewal and the rates dropped $5.00. I asked why so little and they said there were new policies in effect in CA that raised our rates, when I asked by how much they said they didn't know then said it was different for each customer.

I researched new insurance and found Geico charged less than half of what I was paying esurance. They are a ripoff, do not use them!

Car Insurance

In 2004, I had 2 auto accidents that were 2 months apart. Neither were my fault. Esurance stopped my PIP benefits for the 1st when I had the 2nd accident. I guess they felt I had recovered. However, injuries from the 1st got worse with the 2nd car accident. Esurance sent me to 2 independent medical exams. The chiropractor said that I chiropractor could never help me. The 2nd was a pain and rehab dr who said I should go home and exercise. When I did not get better in 2006, I went to a neurosurgeon who told me that I needed 2 surgeries. Esurance has ignored my letters and I have been suffering and in a lot of pain ever since. My back has gotten much worse in those areas and is now described as severe. I have lost my job and my health insurance shortly after the accidents. My boss was not happy that I could not do the same job that I used to do. I have filed a complaint letter with Esurance and plan to file suit on Oct. 20, 2009 if I do not get response this time. These accidents have destroyed my life.

Esurance cut off my benefits after those two exams.

The complaint has been investigated and resolved to the customer’s satisfaction.

This is a terrible company. My policy refund check bounced! http://blog.vshoward.com/2009/06/23/esurance/#content

Terrible company

I started my search for automobile insurance with Geico and after the amount was too high I went to Esurance.com. After i received a quote and my payment was taken, my monthly payment increased two times. I was told that the state of FL by law would not let me cancel with in 60 days and that i would be charged a fee. I could not afford the new payment but i stuck it out and when my 60 days was up i sought more affordable insurance, a 100 dollars a month cheaper to be exact, and canceled the policy with Esurance. They still charged me a 10% cancellation fee after the 60 days of $84 dollars. I would not recommend this insurance company.

The complaint has been investigated and resolved to the customer’s satisfaction.

FL and SC law forbids cancellation within 60 days of inception without proof of duplicate/alternate coverage or other valid reasons.

Check your laws for a list of valid reasons. The insurance company can't "lead" you with the reasons allowed, you have to provide the reason for cancellation. If you buy from company A today @ $1200/six months and next week find a policy from company B for $900.00/six months, then BUY IT! Call company A back and tell them that you have purchased a policy from company "B", provide the company name and policy number and get your refund from company A!

A few bad apples spoiled the WHOLE bucket on that. Too many people were buying a policy, getting the ID cards, and cancelling the policy. They'd have "proof of insurance" in the vehicle, even though the policy was NO LONGER valid! They were driving without insurance, and getting into accidents, leaving the rest of us vulnerable!

It was NOT the insurance companies fault that people were doing that, and the laws were changed for this. It was (some) customers!

In regard to "post purchase rerates" and "cancellation fees":

1. ANYTIME you get a quote/buy a new policy, with ANY COMPANY there is a "discovery period" where the underwriting investigation is done. Most of the time today, with modern technology MVR, Credit, Verification of Previous coverage and Claims reports can be verified at purchase. But, if a state system is down, and the company can't pull the MVR (or other report), and you indicate that you have no accidents, violations or claims, the policy will start with that information.

However, once the MVR, Claims, Credit, or whatever report(s) that may not have been able to be verified at the time of purchase finds "other" information, rerate(s) will occur.

2. If a rerate occurs, and it is the result of an error, contact your insurance carrier for the contact information to dispute the information. Just like errors can occur on credit reports, they can occur on MVR, Claim and other reports that are used to establish the premium owed. You will want to clear that from the current carrier's records, AS WELL AS the reporting agency's records, so that the issue won't be a recurring issue in the future, when you renew and/or purchase a new policy.

3. Granted, not every insurance company charges a "cancellation fee", but it is NOT uncommon. Regardless of which insurance company you do business with, ALWAYS check the terms and conditions. If you accept them, without reading them, you are still legally bound to them. Some states do not allow this, MN, MI, TX, IL, NJ are a few of them... but others will allow for this, and the cancellation fee will either be a "flat fee" regardless of how much time is left before renewal. Other's will allow a percantage of the leftover premium. So, if 50 days of premium left at $5.00/day for $250.00 of premium, then $25.00 cancellation fee deducted from refund, or if only 6 days of premium left at $5.00/day for $30.00 of premium unpaid, then $3.00 cancellation fee. This is especially important to watch if the cancellation fee is a flat rate! If the CX fee is $50.00, but only 2 days of the current term left, at $5.00/day, then you'd owe MORE for cancelling than to keep the policy for two more days.

You need to make the decision, pay $10.00 for two more days of coverage, or cancel early and have $10.00 credit with $50.00 fee, to pay $40.00 more for two days less coverage.

Don't get mad at anyone but yourself for not knowing what is disclosed in declaration pages and terms and conditions, and coverages selected!

It is NOT uncommon for insurance policies to be purchased at "state minimum" liability coverages. In FL, the lowest Bodily Injury Limits without declining the coverage is: $10, 000 per person/$20, 000 per accident cap.

If that is what someone has purchased, even if they are driving a 1984 Ford Escort, and hit someone else who has medical bills as a result of the accident, $10, 000 will be very easily exhausted! If they hit someone and cause $50, 000 in medical bills, but have only purchased $10, 000 in coverage, that driver will still be responsible for $40, 000 in medical bills!

A 1984 Ford Escort can still cause just as much damage/injury as a 2010 Focus, 2010 Chevy, et al.

Liability limits are NOT insuring the vehicle! Liability limits are insuring against the damage/injuries the vehicle can cause!

Call your agent/company to make sure you have enough insurance! One week in the hospital today can easily cost $100, 000! If you only have $10, 000, $25, 000, $50, 000 in liability coverage, you are UNDERINSURED, unless you have a million dollars in the bank! You can be sued, garnished, or have your assets and bank accounts of various types seized in a lawsuit if you don't have enough insurance!

it probably increased b/c you didnt tell them about some activity you had

About Esurance

Esurance Customer Reviews Overview

Here is a guide on how to file a complaint against Esurance on ComplaintsBoard.com:

1. Log in or create an account: Start by logging into your ComplaintsBoard.com account. If you don't have one, create a new account on the website.

2. Navigating to the complaint form: Locate and click on the 'File a Complaint' button on the ComplaintsBoard.com website. You can find this button at the top right corner of the website.

3. Writing the title: Summarize the main issue with Esurance in the 'Complaint Title' section.

4. Detailing the experience: Provide detailed information about your experience with Esurance. Mention key areas such as transactions, steps taken to resolve the issue, company's response, personal impact, etc.

5. Attaching supporting documents: Attach any relevant supporting documents to strengthen your complaint. Avoid including sensitive personal data.

6. Filling optional fields: Use the 'Claimed Loss' field to state any financial losses and the 'Desired Outcome' field to specify the resolution you are seeking.

7. Review before submission: Review your complaint for clarity, accuracy, and completeness before submitting it.

8. Submission process: Submit your complaint by clicking the 'Submit' button.

9. Post-Submission Actions: Regularly check for responses or updates related to your complaint on ComplaintsBoard.com.

Ensure each step is clearly defined to effectively guide you through the process of filing a complaint against Esurance on ComplaintsBoard.com.

Overview of Esurance complaint handling

-

Esurance contacts

-

Esurance phone numbers+1 (800) 378-7262+1 (800) 378-7262Click up if you have successfully reached Esurance by calling +1 (800) 378-7262 phone number 0 0 users reported that they have successfully reached Esurance by calling +1 (800) 378-7262 phone number Click up if you have UNsuccessfully reached Esurance by calling +1 (800) 378-7262 phone number 0 0 users reported that they have UNsuccessfully reached Esurance by calling +1 (800) 378-7262 phone numberCustomer Service

-

Esurance emailscustomerservice@csr.esurance.com100%Confidence score: 100%Supportcustomerfeedback@csr.esurance.com100%Confidence score: 100%

-

Esurance headquarters650 Davis Street, San Francisco, California, 94111, United States

-

Esurance social media

Most discussed Esurance complaints

My car was parked on a city street parking meter in *************Recent comments about Esurance company

My car was parked on a city street parking meter in *************Our Commitment

We make sure all complaints and reviews are from real people sharing genuine experiences.

We offer easy tools for businesses and reviewers to solve issues together. Learn how it works.

We support and promote the right for reviewers to express their opinions and ideas freely without censorship or restrictions, as long as it's respectful and within our Terms and Conditions, of course ;)

Our rating system is open and honest, ensuring unbiased evaluations for all businesses on the platform. Learn more.

Personal details of reviewers are strictly confidential and hidden from everyone.

Our website is designed to be user-friendly, accessible, and absolutely free for everyone to use.

Is ComplaintsBoard.com associated with Esurance?

ComplaintsBoard.com is not affiliated, associated, authorized, endorsed by, or in any way officially connected with Esurance Customer Service. Initial Esurance complaints should be directed to their team directly. You can find contact details for Esurance above.

ComplaintsBoard.com is an independent complaint resolution platform that has been successfully voicing consumer concerns since 2004. We are doing work that matters - connecting customers with businesses around the world and help them resolve issues and be heard.

This concerns us as we have been with Esurance since 2004

I've been an auto insurance customer with esurance for many years, however, all I've ever had to file a claim for was windshield repair, and never had any issues with them on that. I later included renter's insurance on my policy and faithfully paid my premiums for years. Well, on June 8th there was a storm that apparently fried my laptop. I reported the claim to esurance on June 9th. No one ever contacted me. During the end of June I was able to find out Nytozia Scurry (nytozia.scurry@ngic.com) was my adjuster. I kept leaving messages and when she finally called back she said she had been out on bereavement leave, but she was not the adjuster for my claim and was erroneously assigned my file because she works in auto claims, not renters. She would have them correct it and assign to the correct adjuster.

It is now almost September, going on 90 days since I filed my claim and I have called and called and emailed and she is still listed as my adjuster and will not return my calls. Even her supervisor, Christopher Price (christopher.price@ngic.com), will not return my calls. I have now canceled my policies with them and signed on with Allstate. Since esurance is supposed to be a sister company to Allstate I will cancel my Allstate policy if they will not step in and help resolve this. It is not a large claim. Only $1000, and my deductible is $500 so they will only pay $500. I have had to spend more money and purchase the same laptop that I purchased only 15 months prior to the damage.

It seems it is time for a class-action lawsuit against esurance as too many of us are having the same issues with them. I wonder if they are filing bankruptcy. If not, they may have to as they are losing their customers because of this.